Yes. Consolidated sustainability reporting at the EU-level may be required, in addition to the separate sustainability reporting required for all EU companies in scope.

The new EU Corporate Sustainability Reporting Directive (CSRD) seeks to level the playing field for all companies operating in the EU by requiring consolidated sustainability reporting by third-country undertakings with significant activity in the EU, and ensuring that stakeholders have access to transparent and verifiable information.

Third country undertakings

Third-country undertakings are non-EU parent companies which either:

These third-country undertakings are subject to consolidated sustainability reporting requirements on their EU operations from financial year 2028. The required disclosures are tailored to focus on environmental and social impacts, and will be subject to EU reporting standards specific to third-country undertakings. An exemption may apply if the non-EU parent reports sustainability information in accordance with equivalent sustainability reporting standards.

Qualifying branch or subsidiary

A qualifying EU branch is one having net turnover of more than €40 million. A qualifying EU subsidiary is a large company being one that exceeds any two of: 250 employees; €40 million net turnover; or €20 million total assets, or a small or medium-sized entity (SME) with securities listed on an EU regulated market. An SME is a company that exceeds any two of: 10 employees; €700,000 net turnover; or €350,000 total assets.

The qualifying EU branch or subsidiary is responsible for publishing the consolidated sustainability report on behalf of its non-EU parent, on a best efforts basis, and must include a statement if any required information is not provided. The sustainability report must be accompanied by an assurance opinion issued by persons authorised in the third-country of the non-EU parent or in the member state of the qualifying branch or subsidiary.

Illustration

This illustration aims to demonstrate an example of how a non-EU parent group may be brought into sustainability reporting earlier than required in their home jurisdiction – detailed analysis should always be performed to determine the specific application of the EU Sustainability Reporting rules.

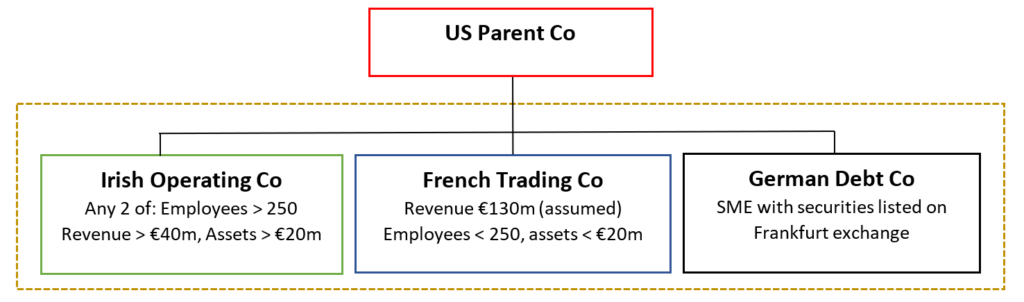

Irish Operating Co – in scope of the CSRD sustainability reporting requirements starting from its 2025 financial year, as it meets the definition of a “large company” due to exceeding at least two of the three size criteria.

German Debt Co – in scope of the CSRD sustainability reporting requirements for SMEs starting from its 2026 financial year with an option to defer to its 2028 financial year, as it has securities listed on an EU regulated market and is assumed to meet the SME size requirements described above.

French Trading Co – not in scope of the CSRD sustainability reporting requirements on its own operations, but it must provide sustainability information to the qualifying EU branch or subsidiary for purposes of EU-level consolidated reporting starting from its 2028 financial year.

US Parent Co – in scope of the CSRD consolidated sustainability reporting requirements on its EU operations from its 2028 financial year, as it meets the third-country undertaking requirements described above. (If US Parent Co had securities listed on an EU regulated market and more than 500 employees, its individual and consolidated reporting obligations would start from its 2024 financial year.)

Ripple effects

The EU sustainability reporting requirements will have ripple effects for other jurisdictions. Decisions taken at EU branch or subsidiary level could impact the wider group’s approach to sustainability. Non-EU parents with substantial operations in the EU are advised to consider carefully their EU sustainability reporting obligations, in good time.

At EisnerAmper we make sustainability simply sustainable.

+353 1 293 3400

+1 212 949 8700

+1 345 945 5889

+65 6305 9900

+353 1 293 3400

+1 212 949 8700

+1 345 945 5889

+65 6305 9900