Complying with the new EU Corporate Sustainability Reporting Directive (CSRD) and the disclosure requirements set out in the (draft) European Sustainability Reporting Standards (ESRS) might seem overwhelming, particularly for businesses that have not previously prepared sustainability reports. In this article, we describe a workflow approach that will assist businesses in meeting their compliance obligations, and help shape their transition towards a more sustainable and circular business model, delivering benefits for their business and other stakeholders.

As a reminder, the CSRD Sustainability Reporting requirements come into effect as follows:

FY 2024 -> Listed companies and other Public Interest Entities with more than 500 employees (currently in scope of the EU Non-Financial Reporting Directive (NFRD) and the Taxonomy Directive)

FY 2025 -> All other ‘large’ companies, i.e. those that exceed any two of the following:

– Net turnover of €40m

– Total assets of €20m

– Average employees of 250

FY 2026*-> Listed SMEs (that are not micro-enterprises), small and non-complex credit institutions and captive insurance undertakings (*with an option to defer until FY 2028)

FY 2028 -> Third country undertakings with significant operations in the EU

(see our previous post on third country undertakings here)

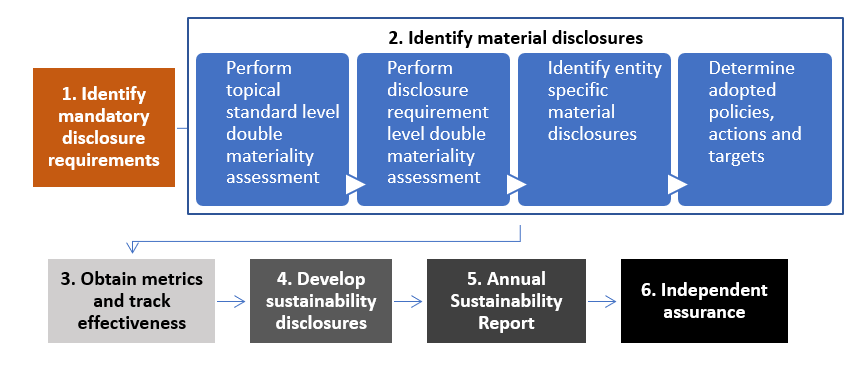

A Sustainability Reporting Workflow

The content of the directive and related standards suggest a logical workflow: starting with the mandatory requirements and working through materiality assessments to develop relevant sustainability disclosures. The steps in a Sustainability Reporting Workflow are summarised in the below diagram and are then addressed under relevant headings.

Sustainability Reporting Workflow

Undertakings must disclose all material information regarding impacts, risks and opportunities in relation to environmental, social and governance matters. What constitutes material information is determined after performing a double materiality assessment, described below. Regardless of the outcome of the materiality assessment, the standards establish certain information to be mandatorily provided by the undertaking:

ESRS 2 – General disclosures covers Disclosure Requirements relating to sustainability governance, strategy and business models, the materiality assessment process, and for policies, actions, targets and metrics regarding identified material topics. Undertakings will need to assess their compliance against these requirements and develop a plan to address any shortcomings / gaps.

EU Law datapoints are embedded in the relevant topical standards, and are tabulated in ESRS 2 Appendix C. They are to be reported irrespective of the outcome of the materiality assessment. Undertakings should, by virtue of addressing the relevant existing legal obligations, already be well positioned to respond to these disclosure requirements and will benefit from the reporting framework and guidance provided by these standards.

ESRS E1 – Climate change covers Disclosure Requirements regarding climate-related hazards that can lead to physical climate risks for the undertaking and its adaptation solutions to reduce these risks. It also covers transition risks arising from the identified adaptation solutions to climate related hazards. These Disclosure Requirements are categorised under: “Climate change mitigation”, “Climate change adaptation” and “Energy”.

Climate change mitigation relates to the undertaking’s endeavours towards holding the increase in the global average temperature to well below 2 °C and pursuing efforts to limit it to 1.5 °C above pre-industrial levels, as laid down in the Paris Agreement.

Climate change adaptation relates to the undertaking’s process of adjustment to actual and expected climate change.

Energy covers requirements related to all types of energy production and consumption.

ESRS S1 – Own workforce itemises certain Disclosure Requirements that are mandatory for undertakings with more than 250 employees. These disclosures include an explanation of the general approach the undertaking takes to identify and manage any material actual and potential impacts on its own workforce in relation to a comprehensive listing of social, including human rights, factors.

Own workforce is understood to include both workers who are in an employment relationship with the undertaking (“employees”) and non-employee workers who are either individuals with contracts with the undertaking to supply labour (“self-employed workers”) or workers provided by undertakings primarily engaged in “employment activities” (NACE Code N.78). Workers in the undertaking’s upstream or downstream value chain are covered in another (not mandatory) standard.

An enterprise conducts a materiality assessment to identify disclosure requirements arising from material impacts, risks and opportunities in the following phases:

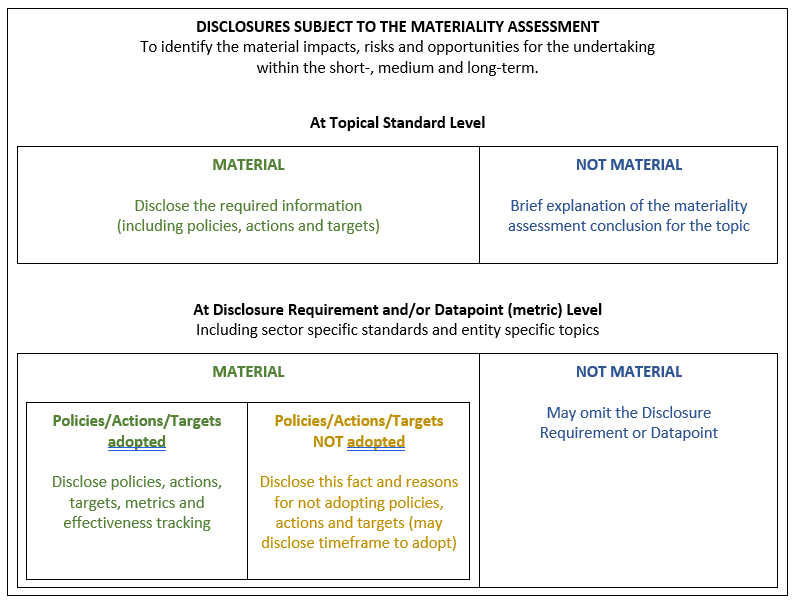

Topical standard level – When a topical standard is assessed not to be material for the undertaking, the undertaking may omit all the Disclosure Requirements in the topical standard. The undertaking shall report a brief explanation of the conclusions of its materiality assessment for the topic. For example, where an in-scope special purpose entity has no employees, it may reasonably conclude that ESRS S1 – Own workforce is not material and therefore omitted entirely, with an appropriate explanation.

Disclosure Requirement level – When a topical standard is assessed to be material for the undertaking, the undertaking shall assess the materiality of all Disclosure Requirements of the relevant standard. When a specific Disclosure Requirement is assessed as not material for the undertaking, the undertaking may omit the specific Disclosure Requirement. For example, where a company does not have non-employee workers (e.g. self-employed contractors), it may reasonably conclude that DR S1-7 – Characteristics of non-employee workers in the undertaking’s own workforce is not material and therefore omitted from the ESRS S1 – Own workforce disclosures.

Entity specific disclosures – When the undertaking concludes that an impact, risk or opportunity not covered or covered with insufficient granularity by a standard is material due to its specific facts and circumstances, it shall provide additional entity-specific disclosures to cover such impact, risk or opportunity. Where the undertaking develops such material entity-specific disclosures it shall report those disclosures alongside the most relevant sector-agnostic and sector-specific disclosures.

Policies, Actions and Targets – If the undertaking cannot provide relevant disclosures on a material sustainability matter because it has not adopted policies and/or actions and/or targets with reference to the specific material sustainability matter concerned, it shall disclose this to be the case, and provide reasons for not having adopted policies and/or actions and/or targets. The undertaking may report a timeframe in which it aims to adopt them.

The table below illustrates the impact of the materiality assessment on sustainability disclosures.

Disclosures subject to the materiality assessment

Applying the double materiality assessment

Performing a materiality assessment is necessary for the undertaking to identify the material impacts, risks and opportunities to be reported. A sustainability matter is material when it meets the criteria defined for impact materiality or for financial materiality. Although impact materiality and financial materiality are inter-related, in general the starting point is the assessment of impacts. A sustainability impact may be financially material from inception or become financially material over time. Material impacts are included irrespective of their financial materiality assessment.

The undertaking determines appropriate thresholds to determine which identified impacts, risks and opportunities are material sustainability matters for reporting purposes.

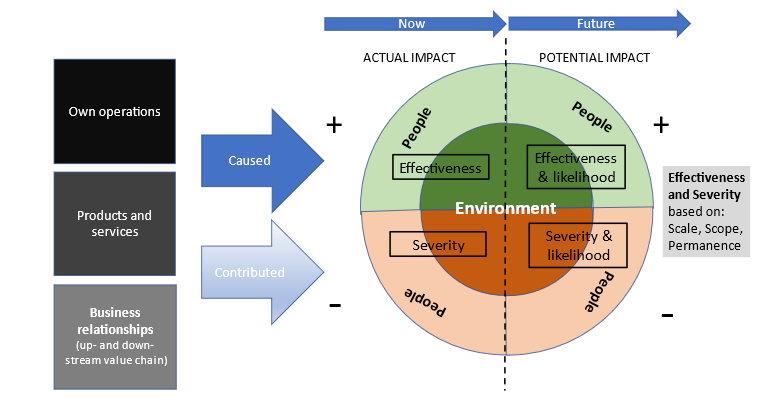

Impact materiality – An undertaking’s material actual or potential, positive or negative impacts on people or the environment over the short-, medium- and long-term time horizons are its material impacts. Impacts include those caused or contributed to by the undertaking and those which are directly linked to the undertaking’s own operations, products, or services, or through its business relationships. Business relationships include the undertaking’s upstream and downstream value chain and are not limited to direct contractual relationships.

Materiality of negative impacts considers the severity of actual negative impacts and the likelihood and severity of potential negative impacts. Materiality of positive impacts considers the effectiveness of actual impacts and the likelihood and effectiveness of potential positive impacts. Severity and effectiveness are assessed based on the scale (how grave or beneficial the impact is), the scope (how widespread the impact is), and permanence (how remediable the negative impact is, or how transient the positive impact is).

The undertaking’s actions to address certain impacts or risks, or to benefit from certain opportunities in relation to an identified material sustainability matter, might itself have material negative impacts or cause material risks in relation to other sustainability matters. For example, action plans to decarbonise own operations by abandoning a plant may have material negative impacts on their own workforce, workers in the value chain or affected communities. In such circumstances, undertakings shall disclose these material negative impacts or risks with a cross-reference to the affected sustainability topic disclosures.

Impact materiality assessment

Engagement with affected stakeholders is central to the undertaking’s ongoing due diligence process to identify actual or potential negative impacts, and to assess and identify material impacts for the purpose of sustainability reporting. Affected stakeholders are individuals or groups whose interests are affected or could be affected – positively or negatively – by the undertaking’s activities and its direct and indirect business relationships across its value chain. Common categories of stakeholders are: employees and other workers, suppliers, consumers, customers, end users, local communities and vulnerable groups, and authorities (including regulators, supervisors and central banks). Nature may be considered a silent stakeholder.

Financial materiality – The scope of financial materiality for sustainability reporting is an expansion of the scope of materiality used in the process of determining which information should be included in the undertaking’s financial statements. A sustainability matter is material from a financial perspective if it triggers or may trigger material financial effects on the undertaking, including: cash flows, development, performance, position, cost of capital or access to finance in the short-, medium- and long-term time horizons.

Risks and opportunities may derive from past or future events and may impact:

The financial materiality of a sustainability matter is not constrained to matters that are within the control of the undertaking but includes information on material risks and opportunities attributable to business relationships with other undertakings/stakeholders beyond the scope of consolidation used in the preparation of financial statements.

The materiality of risks and opportunities is assessed based on a combination of the likelihood of occurrence and the size of the potential financial effects.

The Disclosure Requirements contained in the standards prescribe disclosure content regarding Policies, Targets, Actions, and Metrics related to a specific sustainability matter:

Policies – refer to general objectives or management decisions implementing the undertaking’s strategy towards a material sustainability matter.

Targets – refer to measurable, outcome-oriented goals that the undertaking aims to achieve.

Actions – including action plans and transition plans, are implemented to ensure that the undertaking delivers against the policies and targets.

Metrics – are qualitative and quantitative indicators that the undertaking uses to measure and report on effectiveness of delivery against policies, targets and actions over time.

For most Disclosure Requirement sets, the standard prescribes the relevant metrics. For example, ESRS E1 Climate Change DR E1-5 Energy consumption and mix requires disclosure of total energy consumption in MWh related to own operations across 6 categories of non-renewable sources and 3 categories of renewable sources, and where applicable, the disaggregated renewable and non-renewable energy production. In some cases, identifying and obtaining the relevant datapoints will involve reference to sector-specific or cross-sector methodologies, such as the Science-based Target Initiative.

For each metric the undertaking shall describe how the metric is used to track effectiveness, shall use clear and precise names and descriptions, and disclose whether the metric is externally validated. Information presented should be disaggregated for a proper understanding of the material sustainability matter, by country or region, by sector, or by site or significant asset.

Past, present and future is linked by presenting one year of comparative information for all metrics disclosed in the current year, and reporting against a base year, and where relevant presenting forward-looking information, for an understanding of progress towards targets.

The use of reasonable assumptions and estimates, including scenario or sensitivity analysis, is an essential part of preparing sustainability-related metrics and does not undermine the usefulness of the information, provided that the assumptions and estimates are accurately described and explained. Even a high level of measurement uncertainty would not necessarily prevent such an assumption or estimate from providing useful information or meeting the qualitative characteristics of information.

The (draft) ESRS 1 – General requirements standard provides guidance on the content and structure of the sustainability statements, including a non-binding example structure. The standard expects all required sustainability disclosures to be in a single section of the company’s management report, which accompanies its annual financial statements. Information already provided in another part of the sustainability report or elsewhere in the company’s financial statements, management report, corporate governance report or remuneration report, may be included by reference to avoid duplication.

Relationships between information in the sustainability statements and other information in the annual report must be described clearly and concisely, to illustrate consistency of data and assumptions. Sustainability disclosures and datapoints must be linked with specific references to relevant paragraphs and include reconciliations for financial or other quantitative data.

For example, sustainability targets for reducing use of natural resources may need to be linked to the strategic response to limit impact through related investments in new assets or divesting of existing assets. This information may also need to be reconciled with financial statement metrics on production costs and related financial performance targets.

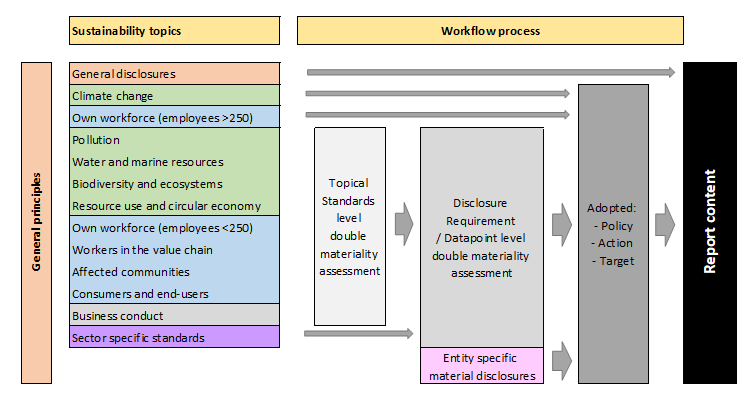

The Sustainability Reporting Workflow and Double Materiality assessment process is illustrated in the below diagram:

Developing disclosures for material sustainability matters

Drawing up and publishing information in compliance with the sustainability reporting standards is the collective responsibility of the members of the administrative, management and supervisory bodies of an undertaking, as an extension of their responsibilities for financial statements and other management reports.

The standards require an undertaking to disclose how the administrative, management and supervisory bodies are informed about sustainability matters and how these matters were addressed during the reporting period. An undertaking shall also disclose information about the integration of its sustainability-related performance in incentive schemes and how the interests and views of its stakeholders are taken into account.

The sustainability report shall be accompanied by an assurance opinion expressed by a person or firm authorised to give an opinion as regards the compliance of the sustainability reporting with the requirements of the CSRD, including the compliance of the sustainability reporting with the sustainability reporting standards to be adopted (the ESRSs). (See our previous post on the assurance requirements here.)

Start here, start now!

Preparing for your first Annual Sustainability Report for FY 2024 (listed and other public interest entities) or FY 2025 (other ‘large’ companies) will require careful and thorough planning. Following a governance-based structured sustainability reporting workflow will ensure that your sustainability report is:

At EisnerAmper we make sustainability simply sustainable.

The content above is provided for general information purposes only and is not intended to provide, nor does it constitute, professional advice on any particular matter. If you would like more information or would like to discuss any of the topics raised above, please contact the author(s).

The content above is provided for general information purposes only and is not intended to provide, nor does it constitute, professional advice on any particular matter. If you would like more information or would like to discuss any of the topics raised above, please contact the author(s).

+353 1 293 3400

+1 212 949 8700

+1 345 945 5889

+65 6305 9900

+353 1 293 3400

+1 212 949 8700

+1 345 945 5889

+65 6305 9900