Ireland is building world-class startups. The scaleup chapter is harder to write.

Earlier this month, Salesforce signed a definitive agreement to acquire Fin, formerly Intercom, for approximately $3.6 billion. If completed, it will be widely regarded as the largest exit for an Irish-founded technology company.

It’s worth pausing on what that represents. A business that started in a Dublin coffee shop in 2011 became one of Ireland’s first unicorns, scaled into a global category-definer, and is now set to join one of the most acquisitive software companies in the world. The company may be headquartered in San Francisco, but it kept a substantial base in Dublin throughout. Its founders remain closely connected to the Irish ecosystem, and a generation of Irish employees will now share in the outcome.

That is exactly the kind of scaleup chapter Ireland needs more of. It is also a useful lens through which to read a quieter set of numbers that landed a few weeks earlier.

The IVCA’s VenturePulse report for Q1 2026 landed recently, and one number has dominated the conversation: €221.7m in venture funding into Irish SMEs, down significantly across most deal sizes. In a climate already shaped by global uncertainty, tariff turbulence and tightening investor discipline, it is tempting to read that as a warning sign. I would encourage a more careful read.

Investment in transactions below €1m increased quarter on quarter. The deals that did close tell a story of genuine, world-class Irish innovation: Neurent Medical raising €62.5m; Aerska closing €33m in biotech; and Evervault securing €21m in cybersecurity, with Sequoia and Ribbit Capital at the table. Deals like these do not happen by accident. They are not flukes. They are proof that Irish founders are building companies that compete globally. The funding market has not broken. It has become more disciplined. That is a different problem, and in some ways, a more useful one to solve.

The gap that the numbers don’t show

What the IVCA data captures is activity. What it does not capture are the companies that did not make it to a funding round at all: the ones that stalled between Series A and Series B, or that raised early but could not convert momentum into the kind of operational maturity that serious investors now demand.

That is the scaleup gap. And it has been hiding in plain sight for years.

Ireland has long been acknowledged as a strong environment for early-stage companies. Enterprise Ireland, the accelerator ecosystem, and a genuinely collegiate founder community have created real energy at the start of the journey. Successive government reports and commentators point to the same fault line: Irish companies often lose ground at scale. They get acquired earlier than they might otherwise, relocate to access deeper capital markets, or simply plateau.

The conversation tends to focus on capital availability, and rightly so. Better access to growth capital, particularly at Series B and beyond, matters. The constraint has never been a shortage of Irish capital, it’s the absence of sufficient incentives and structures to put it to work, which is particularly frustrating with roughly €170 billion sitting in low-yield deposits while ambitious companies struggle to close Series B rounds. Encouragingly, that gap is now firmly on the policy agenda, through a planned retail investment account to mobilise household savings, dedicated SME scaling funds, and a sharper Enterprise Ireland focus on later-stage capital. The direction is right; the imperative however is to go further and faster. But in my experience, the barrier is often not just capital. It is the infrastructure around the business.

What investors are scrutinising right now

The era of growth at all costs is over. That shift has been well documented globally, but its implications for Irish founders are still being absorbed.

In a more selective market, investors are spending longer on diligence. They are asking harder questions, not just about the product or the market, but about the business behind the business. Can the leadership team articulate its unit economics clearly? Is the financial reporting investor-grade, or is it held together with spreadsheets and goodwill? Is there a credible person at the table who can answer the CFO-level questions when they come?

These are not unreasonable asks. They are the basics. But for many brilliant founders who have been rightly focused on product and customers, building that financial infrastructure has been deferred. It feels like a problem for later. Until later arrives.

The lesson I would draw from the companies that closed meaningful rounds in Q1 is not simply that quality still gets funded. It is that preparedness now matters more. That distinction matters more now than it did two years ago.

The structural question for Irish founders

There is a broader point worth making here, one that goes beyond any individual company.

Ireland is at an interesting moment. The FDI model that underpinned so much of our economic growth remains a major national strength, but the strategic case for building genuinely indigenous, scaling Irish companies has become harder to ignore. Scale Ireland, Enterprise Ireland and others are making that argument loudly and rightly.

But ambition without infrastructure is just aspiration. If Ireland is serious about developing a cohort of scaling companies that stay Irish, grow Irish jobs and compete on the global stage, then the ecosystem around those companies needs to mature alongside them. That means better access to growth capital at Series B and beyond. It means more experienced operator-advisers who have actually sat inside scaling businesses. And it means founders taking financial credibility as seriously as product credibility earlier than feels necessary.

What the Fin deal tells us about the scaleup chapter

Intercom did not become acquirable by accident. Over recent years, the company made hard, decisive choices: repricing its core product, walking away from revenue it had previously banked, and committing early and fully to AI while the direction of the market was still uncertain. That is operational discipline at the sharp end: the willingness to rebuild the business around where the market is going rather than where it has been. It is the same quality, seen at an earlier stage, that investors now look for in companies a fraction of the size.

It is also a more complicated story than a simple Irish success. The company moved its headquarters to San Francisco to reach the capital and customers it needed, and the proposed outcome is a sale to a larger US acquirer. This is the pattern that has shaped Irish scaling for two decades. What is different is the scale at which it happened, and what it leaves behind: a deep bench of operators who have now built and sold at the highest level, and a cohort of employees whose payouts will, if past cycles are any guide, seed the next wave of Irish founders and angel investors.

That recycling of talent and capital is how ecosystems mature. It is the part of the story that outlasts any transaction.

A more honest conversation

The Q1 IVCA numbers are far from a crisis. But they are a prompt.

For founders in growth mode, the question is not whether the funding market has changed. It has. The question is whether your business is being built to meet it. The companies that will define the next chapter of Irish enterprise will not just have great ideas. They will have the operational discipline and financial clarity to make investors confident that their capital will be well deployed.

That is not a new standard. It is just one that is being enforced more consistently than before.

Fin’s proposed acquisition is a milestone worth celebrating. The real prize is a pipeline of companies built well enough to write many more chapters like it.

To continue the conversation, please contact:

Stephen Kinch, Partner, Head of Scaling Services

Stephen.Kinch@eisneramper.ie

or +353 85 818 6801

Stephen Kinch

Carmanhall Road

Sandyford

Dublin, D18 CA22

Ireland

Financial Resilience Is No Longer Optional. It Is Strategic.

In today’s environment, uncertainty is not a disruption to normal business conditions. It is the operating environment.

Geopolitical instability, macro-financial volatility, market disruption, cyber threats, and operational risks are no longer episodic. They are continuous, interconnected, and increasingly complex. Risks that once emerged gradually can now materialise within weeks, reshaping market conditions, client behaviour and business performance.

For Irish MiFID firms, this reality is reflected clearly in the Central Bank of Ireland’s 2026 supervisory priorities, with a strong emphasis on maintaining and strengthening resilience to geopolitical and macro-financial risks.

Against this backdrop, financial resilience has evolved from a focus on regulatory compliance and capital adequacy to a broader capability: the ability to

withstand shocks, adapt quickly, and continue operating in a safe and orderly manner without compromising clients, markets, or long-term viability.

From Compliance to Capability

Historically, resilience was often viewed through a narrow operational lens such as business continuity plans, system availability, and disaster recovery arrangements.

While these remain important, today they are no longer sufficient on their own.

Financial resilience sits at the core of a firm’s ability to function under stress. Without it, firms cannot effectively:

- Absorb prolonged revenue shocks

- Manage liquidity pressures

- Maintain client confidence

- Respond strategically to disruption

In many respects, financial resilience underpins every other form of resilience.

Crucially, regulators are increasingly assessing resilience not just through financial metrics, but through the quality of governance, the credibility of planning, and the strength of the decision-making frameworks that support firms through periods of uncertainty.

What Firms Are Telling Us

During a recent webinar hosted by EisnerAmper Ireland in conjunction with the IMIA, we asked participants about the maturity of their financial resilience frameworks.

The findings reveal a sector that is highly aware of emerging risks and actively engaged in addressing them but still progressing towards fully embedded resilience capabilities.

- Board engagement is improving but not yet dynamic.

Encouragingly, most firms reported that their Boards have considered geopolitical risk within the past year, with many doing so in the previous six months.

This represents meaningful progress. Boards increasingly recognise that geopolitical developments are no longer peripheral concerns; they are material drivers of financial performance, strategic risk and organizational resilience.

However, the findings also raise an important challenge.

In today’s environment, risk profiles can change rapidly. Energy market volatility, interest rate movements, cyber incidents, trade disruption and geopolitical conflict can alter a firm’s financial outlook in a relatively short period.

As a result, resilience requires more than periodic review. It requires continuous

oversight, challenge and recalibration.

The most resilient firms are moving beyond annual risk discussions and incorporating resilience considerations into regular Board decision making and strategic planning.

- Awareness is high, but embedding remains limited.

When firms were asked whether they had updated their ICAAP or ICARAP frameworks to reflect geopolitical developments, a clear pattern emerged.

While a small number of firms have fully embedded resilience considerations into their operating models, many remain in earlier stages of maturity. Some are still

- Exploring the impact

- Running limited pilots

- Or implementing changes in specific business areas only

This gap matters.

ICAAP and ICARAP processes are intended to be dynamic, forward-looking, and integrated into strategic decision-making. Yet for many firms, they continue to operate primarily as annual regulatory exercises rather than living management frameworks.

The result is often a disconnect between recognising risk and responding to it in a structured and enterprise-wide manner.

As supervisory expectations continue to evolve, this gap will become increasingly difficult to sustain.

The Real Risk: Strategic Drift

One of the most important and often underestimated insights from this discussion is that financial fragility rarely arises from a single event.

More often, it stems from gradual strategic drift, including:

- Overreliance on a small number of clients or revenue streams

- A cost base that cannot flex under pressure

- Business plans based on outdated market assumptions

- Slow or ineffective decision-making processes

- Insufficient challenge around emerging risks

Individually, these issues may appear manageable. In stable environments, they may go largely unnoticed.

However, in stressed conditions, they can quickly become critical vulnerabilities.

This is why financial resilience cannot be treated as a compliance exercise alone. It requires strategic honesty and a willingness to challenge the long-term sustainability of the business model, not simply its regulatory position.

What ‘Good’ Looks Like

The direction of travel from regulators is unambiguous.

Stronger firms are already moving beyond baseline compliance and demonstrating a more mature approach to resilience through:

- Active Board ownership of financial resilience, supported by regular and data-driven challenge

- Severe but plausible stress testing that informs real business decisions

- Robust liquidity management, including forward-looking cash flow analysis and contingency planning

- Integrated resilience frameworks linking financial, operational, and strategic risks

- Credible recovery and wind-down planning grounded in realistic scenarios

- Clear management information that supports timely and effective decision making

Importantly, these firms are not attempting to predict the future perfectly.

Instead, they are building the capability to respond effectively regardless of what the future brings.

Turning Resilience into Competitive Advantage

Resilience is often viewed through a defensive lens, something necessary to satisfy regulatory expectations and avoid adverse outcomes.

That perspective overlooks a significant strategic opportunity. Firms that invest meaningfully in financial resilience are better positioned to:

- Navigate volatility with confidence

- Maintain and strengthen client trust

- Act decisively when competitors cannot

- Capitalise on market dislocations when competitors are constrained

In an uncertain environment, resilience becomes more than a protective mechanism. It becomes a source of competitive advantage.

Where Firms Go from Here

The findings from our discussion point to a clear conclusion.

The industry is moving in the right direction, but many firms have not yet reached full maturity.

The challenge is no longer awareness. It is execution.

Embedding financial resilience requires a structured and end-to-end approach that connects governance, risk management, capital planning, liquidity management, and business strategy within a coherent framework.

It also requires firms to move beyond static assessments and adopt a more continuous, forward-looking approach to decision-making.

How EisnerAmper Ireland can help

As firms seek to strengthen their resilience capabilities, an objective assessment can help identify gaps, prioritise actions and align resilience planning with both regulatory expectations and business strategy.

EisnerAmper Ireland supports Irish MiFID firms in designing, assessing and embedding financial resilience frameworks aligned to:

- Central Bank of Ireland expectations

- ESMA guidance

- MiFID II, IFR and IFD requirements

Our support typically focuses on two key areas.

- Benchmarking and Diagnostic

We assess the current state of your financial resilience framework across:

- ICAAP and ICARAP frameworks

- Stress testing and scenario design

- Liquidity risk management

- Governance and Board oversight

- Recovery and wind-down planning

This provides a clear view of how resilience is currently documented, understood, and applied in practice.

- Actionable Implementation

We work with firms to develop prioritised and practical action plans that:

- Address identified gaps

- Strengthen forward-looking risk management

- Enhance Board reporting and decision-making

- Integrate resilience considerations into strategic planning

Our focus is on helping firms move from intention to implementation and from compliance to capability.

Final Reflection

The question facing firms today is not whether disruption will occur.

It will.

The real question is whether firms are prepared,

financially, operationally, and strategically, to withstand it.

Those that are will do more than survive periods of uncertainty.

They will be positioned to lead through them.

If these challenges resonate with your firm, now is the time to move from reflection to action and assess whether your resilience framework is truly prepared for an increasingly uncertain environment.

To continue the conversation, please contact:

Ronan Murphy, Partner, Head of Internal Audit – Ronan.Murphy@eisneramper.ie or +353 1 2933 432

Frank Keane, Partner, Governance, Risk & Compliance – Frank.Keane@eisneramper.ie or +353 1 2933 450

Author

EisnerAmper Ireland appoints Julian Yarr as Non-Executive Chair

EisnerAmper Ireland is pleased to announce the appointment of Julian Yarr as non-executive Chair of its Board.

The appointment reflects the continued evolution of EisnerAmper Ireland as it strengthens its position as a specialist advisory and accounting firm, serving clients in the financial services, international trade and government sectors.

Recognised as one of Ireland’s most respected leaders in professional services, Julian Yarr brings a wealth of corporate experience to the Board of EisnerAmper Ireland. His distinguished career includes leadership of one of the country’s largest law firms, board advisory and corporate governance roles.

A corporate lawyer by profession, Julian spent more than 25 years with A&L Goodbody, one of the largest and leading law firms in Ireland. He held a number of senior leadership positions at the firm throughout his career, before being appointed managing partner in 2010 – a position he held for 12 years. At the same time, Julian also served as a member of the Advisory Board of Accenture in Ireland for over a decade.

He also brings significant international governance experience through senior advisory coaching and board roles across the UK and Europe, including as independent Chair of the Board of Sorainen, the leading law firm in the Baltics, as Chair of the board of Social Entrepreneurs Ireland and as independent board advisor to Advant, one of the largest independent European law firm alliances.

He is a previous member of the Advisory Board of the Law Firm Management Committee of the International Bar Association and is accredited by the European Mentoring and Coaching Council as a leadership coach.

As Chair, Julian will provide independent strategic oversight and governance leadership to the Board of EisnerAmper Ireland, supporting the Firm’s continued growth ambitions both in Ireland and internationally.

Commenting on his appointment as Non-Executive Chair of EisnerAmper Ireland, Julian Yarr said:

“What attracted me to EisnerAmper Ireland is the clarity of its vision, strategic positioning and the quality of its leadership. This is a firm that has chosen to specialise deeply in sectors where experience, judgement and relationships matter. It has an exceptional entrepreneurial culture, brings an international focus to Ireland and is well ahead of the curve on the development and deployment of AI and other technologies.”

“Having observed many firms, I can say that EisnerAmper Ireland has a true partner-led client service model. This means that clients are assured of quality by working directly with senior leaders who understand both the technical and commercial realities of their industries and provide premium, practical and responsive advice.”

“EisnerAmper Ireland has already built something distinctive in the market. It is ideally positioned to lead through an exciting and challenging period of change for clients and the profession. I look forward to working with the partners and leadership team as the Firm continues its next phase of growth and expansion.”

Attracta van Rensburg, CEO of EisnerAmper Ireland, commented:

“Julian’s appointment is an important milestone for EisnerAmper Ireland as we continue to grow as a specialist firm built around deep sector expertise, senior-led client service and commercially grounded advice.”

“We have been deliberate in building a partnership group with significant experience in the sectors we serve. That focus continues across the wider Firm as we invest in attracting and developing high-calibre talent with deep sector expertise and experience. Our clients value direct access to our Partners who understand the complexity of their markets, the commercial realities of scaling across jurisdictions and can provide clear, practical advice in fast-moving, regulated environments.”

“Julian brings exceptional experience in leading complex professional services organisations and a deep understanding of what makes specialist partner-led firms successful. His insight, judgement and international perspective will be of enormous value as we continue to scale the business.”

Latest News →

EisnerAmper Ireland Announced as Advisory Partner to Tech Tee Up for Charity

EisnerAmper Ireland is proud to announce its appointment as Advisory Partner to Tech Tee Up for Charity, a unique initiative uniting Ireland’s leading tech founders, investors, and scaling community in support of three outstanding causes: Our Lady’s Hospice & Care Services, Children’s Heartbeat Trust, and Just ASK.

The event highlights the strength of Ireland’s scaling ecosystem, bringing together innovators and investors who are driving high-growth businesses, while working towards an ambitious fundraising goal of €150,000 for charity.

Commenting on the partnership, Stephen Kinch, Partner and Head of Scaling Services at EisnerAmper Ireland, said:

“Events like Tech Tee Up combine purpose with ambition, bringing great people together with a clear goal. We are truly honored to support the event and the organising team. I’d encourage anyone interested to sign up to the limited remaining slots. It promises to be a great day of connection for exceptional causes.”

At EisnerAmper Ireland, we work closely with scaling and high-growth businesses across Ireland, supporting them through each stage of their journey. Partnering with initiatives like Tech Tee Up for Charity reflects our commitment to supporting both the business community and the wider society it serves.

We are delighted to collaborate with fellow partners including eDesk, Needl, Philip Lee LLP, Amplifi, Stripe, and Elkstone, and look forward to contributing to a successful and impactful event.

Latest News →Better Together? Reflections from CUMA 2026

As Irish credit unions face growing regulatory expectations, rising technology costs and increasing competition from banks and fintechs, strategic mergers are becoming less about survival and more about future-proofing the sector.

That was one of the central themes explored at the recent CUMA Conference, where an expert panel tackled the question: “Better Together? Credit Union Strategic Mergers & Learnings from Other Sectors.”

Moderated by Diarmaid O’Keeffe of EisnerAmper Ireland, the panel featured Noel Cunningham of New Era, Carmel Butler of St. Canice’s Credit Union, and Alan Werlau of Barclays. Collectively, the panelists brought extensive merger experience from both the credit union and wider financial services sectors.

Noel has project-managed 60 credit union transfers of engagement over the past 15 years, Carmel was actively involved in eight mergers at St. Canice’s between 2015 and 2020, and Alan has advised on banking consolidations in Venezuela, Chile, the US and Spain.

Their message was clear: credit unions can be “better together” but only if mergers are pursued for the right strategic reasons and executed carefully to preserve each organisation’s culture, strengths and community focus.

Why Strategic Mergers are Increasing

The discussion highlighted that credit union consolidation is increasingly being driven by strategy rather than necessity. Healthy credit unions are now pursuing mergers to build more resilient, member-centric organisations, with greater capacity to invest in people, technology, risk management and systems. The panel noted that the Central Bank of Ireland’s revised due diligence terms of reference for credit union mergers further reinforces the need for rigorous planning, oversight and governance in these strategic combinations.

The Benefits of Scale

One message came through consistently: Scale matters.

By merging, credit unions can benefit from stronger finances, larger and more diversified loan books, greater operational efficiencies and a broader membership base.

Greater scale can also support

- Increased investment in digital services and technology that can attract younger members

- More competitive products

- Stronger risk management and compliance capabilities

- Greater ability to maintain sustainable branch networks allowing local communities to keep access to face-to-face services

- Enhanced career development opportunities for staff.

The panel also observed that larger, well governed credit unions are often better positioned to innovate and meet increasing regulatory expectations.

What Makes a Merger Successful

The panel emphasised that successful mergers require more than financial logic, execution is key.

Credit unions need to identify genuine synergies and be able to deliver them, combining the best of both organisations, including products, people, systems and processes to create an entity that is stronger than the sum of its parts.

Community focus was highlighted as a critical success factor. Keeping branches open where practical, maintaining local engagement and continuing community funding initiatives can help sustain member trust and confidence after a merger.

Communication was another recurring theme. Staff and members need clear, consistent communication throughout the process to build understanding, reduce uncertainty and create buy-in.

Cultural alignment was also identified as essential. Drawing on her experience, Carmel Butler noted that cultural considerations require significant effort before, during and after a merger to ensure employees and members continue to feel engaged and valued.

In practice, this means addressing employee concerns and proactively blending the organisational cultures. Noel Cunningham added that any “soft anxiety” within teams should be acknowledged and proactively addressed throughout the process.

The panel also advised that even thriving credit unions would be wise to have a potential merger “plan B” in place as a contingency, should the operating environment change.

Risks and Pitfalls to Avoid

The panelists shared several cautionary tales.

Rigorous due diligence is essential to uncover financial, operational or governance issues that could undermine a merger.

Member approval remains another key consideration. While rejections are less common than in the past, the panel noted that strong communication and a clearer member value proposition remain critical in securing member support.

The panel also acknowledged that some mergers may need to be abandoned, even late in the process after months of planning. As Noel remarked that “it’s never too late to make the right decision”. In some cases it is better to step away late in the process than to force a partnership that isn’t truly in the best interest of both organisations.

What Comes Next for the Sector

The panel predict that consolidation will continue, resulting in fewer but larger Irish credit unions in the coming years.

Alan Werlau, offering a global perspective, noted that as regulatory requirements and member expectations continue to rise, strategic mergers are likely to become an increasingly important tool for credit unions to remain competitive.

By growing in scale, credit unions can become a stronger collective force in financial services, better able to compete with banks and fintechs while still focusing on their communities.

The panelists also anticipated the rise of new collaborative structures such as Credit Union Service Organisations (CUSOs) and Corporate Credit Unions, allowing groups of credit unions to share services and achieve scale benefits without necessarily merging.

Ultimately, the panel made a compelling case that strategic mergers, when pursued for the right reasons and managed with care, can strength the sector. For many credit unions, the question is no longer whether strategic partnerships should be considered, but when and under what conditions can they create the greatest value for members, staff and communities.

Contact EisnerAmper Ireland

Thinking about a strategic merger?

All credit unions’ circumstances are different. If you are considering a merger or simply want to explore your strategic options, contact Diarmaid O’Keeffe, Partner and Head of Credit Union Services, for a confidential discussion on what the right path could look like for your organisation.

Authors

The content above is provided for general information purposes only and is not intended to provide, nor does it constitute, professional advice on any particular matter. If you would like more information or would like to discuss any of the topics raised above, please contact the author(s).

New Partner Appointments at EisnerAmper Ireland

EisnerAmper Ireland today announced the appointment of Stephen Kinch as Partner, Head of Scaling Services and Siobhan Vickers as Partner, Audit further strengthening the Firm’s senior leadership team.

Stephen Kinch has extensive expertise in scaling high-growth businesses and building agile finance functions to support ambitious expansion plans. He brings practice and senior finance leadership to his role, most recently as CFO of Moby. In his role as Head of Scaling Services, Stephen will lead the continued development of EisnerAmper’s Scaling Services offering, supporting scaling enterprises with finance transformation, fractional CFO and advisory services.

Siobhan joins the Firm with more than 20 years audit experience, leading complex engagements for Irish and multinational companies across the pharmaceutical, technology and hospitality sectors. She previously worked with PWC’s Foreign Direct Investment Group, coordinating large multinational audits across Europe and the US. Her appointment further enhances the Firm’s audit capability and reinforces its commitment to quality, technical excellence and partner-led client service.

Stephen Kinch, Partner, Head of Scaling Servicers, EisnerAmper Ireland, commented:

“I am delighted to join EisnerAmper Ireland at this exciting time for scaling businesses operating from Ireland. Innovation, design thinking and partner led client service are in the DNA of EisnerAmper, this combined with its ability to support organisations across the full finance function makes it a natural choice for growth-focused scaling enterprises.

Access to the EisnerAmper global network further strengthens the proposition for Irish based organisations seeking agile, locally delivered finance leadership. I look forward to working with clients on their scaling journey and to further developing this service within the Firm”.

Siobhan Vickers, Partner, Audit, EisnerAmper Ireland, commented

“EisnerAmper Ireland has built a strong reputation for technical excellence, client service and talent development. It is exceptionally committed to promoting learning and development at all levels. As the profession continues to evolve, firms must prioritise quality management and innovation to deliver effective services and solutions. EisnerAmper is embracing this opportunity.

I am very pleased to be joining such a progressive Firm and look forward to collaborating with my fellow partners and our talented team to continue delivering quality audits for our clients.”

EisnerAmper Ireland CEO, Attracta van Rensburg, commented:

“We are delighted to welcome Stephen and Siobhan to the Firm. These appointments reflect our continued investment in senior leadership capability as part of our long-term growth strategy.

Ireland is exceptionally well positioned as a base for high growth and internationally focused organisations. Under Stephen’s leadership, we are expanding our Scaling Services offering to provide agile fractional CFO and finance advisory solutions tailored to scaling enterprises.

Siobhan’s appointment further strengthens the depth and experience within our Audit practice, reinforcing our commitment to partner-led client service. We are proud to attract senior leaders of this calibre and look forward to the contribution they will make to our Firm and our clients.”

About EisnerAmper Ireland

EisnerAmper Ireland is a specialist firm of accountants, auditors, tax advisors and risk and regulatory experts, with a niche focus on financial services and international trade.

Working alongside 4,000 professionals globally, EisnerAmper Ireland’s 14 Partners and 120+ professionals play a key role in supporting international trade in and through Ireland and in advising Irish corporates.

EisnerAmper Ireland is a founding member of EisnerAmper Global, a New York headquartered specialist network of independent member firms operating across key global international trading and financial services hubs.

Latest News →

Central Bank of Ireland: Key Supervisory Priorities for Credit Unions in 2026

The Central Bank of Ireland (CBI) has published its 2026 Regulatory & Supervisory Outlook (2026 Outlook) outlining the key risks across the financial system and the supervisory priorities that will guide its work in the year ahead. We highlight some of the key cross-sectoral supervisory priorities from the 2026 Outlook here including:

- Resilience under pressure;

- Consumer and Investor protection;

- Technology and digital change;

- Climate and the long-view; and

- What this means for firms.

In relation to Credit Unions, supervisory priorities in 2026 include:

Financial resilience: Reserves and liquidity across the sector remain strong; however, low loan-to-asset ratios continue to present a longer-term sustainability concern. Credit unions availing of the expanded house and business lending framework are expected to do so gradually and prudently. The Central Bank will continue to closely monitor liquidity and asset and liability management (ALM) across the sector.

Business model and strategy: Credit unions are expected to demonstrate progress on digitalisation and sectoral collaboration. Consolidation in the sector, including through transfer of engagements, continues to be encouraged. The Central Bank will progress a regulatory framework for shared service organisations during 2026 and begin policy formulation for corporate credit unions.

Consumer protection, risk management and governance: The revised Consumer Protection Code (CPC) comes into effect in March 2026. The 2026 Outlook notes that the consultation paper on applying the CPC to all regulated credit union activities (CP165) closes in March 2026, with regulations intended to be published by the end of Q3 2026.

In advance of this, the Central Bank expects credit unions to manage conduct risk effectively and demonstrate that members’ interests are protected, while ensuring that risk management frameworks, control environments and operational capabilities continue to mature in line with their product and service offerings and the wider risk environment.

How EisnerAmper Ireland can help

EisnerAmper Ireland’s Governance Risk and Compliance team works with regulated firms at every stage of the regulatory lifecycle, from authorisation through to ongoing supervisory engagement. We closely monitor regulatory developments, including the Central Bank’s annual Regulatory and Supervisory Outlook, as part of our commitment to ensuring clients remain informed, prepared and resilient.

If you would like to discuss how the 2026 supervisory priorities impact your firm, please get in touch.

Authors

Central Bank of Ireland Sets Out Supervisory Priorities for 2026

The Central Bank of Ireland has published its 2026 Regulatory & Supervisory Outlook, outlining the key risks across the financial system and the supervisory priorities that will guide its work in the year ahead.

This is the third year of the report, which is framed against a “rapidly changing international environment characterised by geopolitical tensions, macro-financial uncertainty, technological disruption and climate transition.” While the financial system is described as resilient, the emphasis is on sustaining that resilience through strong governance, effective risk management and operational preparedness.

For regulated firms, the overarching message is clear: regulatory frameworks must be fully embedded and sufficiently robust to respond to this increasingly complex risk landscape.

Below we highlight some of the key cross-sectoral supervisory priorities from the 2026 Outlook:

Resilience Under Pressure

Operational and cyber risks remain central supervisory priorities. The Central Bank highlights the elevated risk environment arising from increasing operational complexity, accelerating digitalisation and firms’ reliance on critical third-party ICT providers.

In 2026, supervisory engagement will include Digital Operational Resilience Act (DORA) implementation, with particular reference to gaps identified in ICT risk management frameworks, governance, third-party oversight and incident reporting practices. Supervisory scrutiny will continue to centre on firms’ preparedness for operational disruption and the ability to maintain continuity of critical services.

From a financial resilience perspective, supervisory focus will remain on credit, liquidity, market stability alongside the sustainability of underlying business models. The report also highlights the growing significance of non-bank financial institutions and interconnected market exposures within the broader risk landscape.

Consumer and Investor Protection

Consumer and investor protection remains central to the supervisory agenda. The revised Consumer Protection Code (CPC), effective from March 2026, will form a central component of supervisory engagement across sectors.

Supervisory work will examine firms’ day-to-day treatment of customers, including complaints handling, management of conflicts of interest, the quality and clarity of client disclosures and products’ governance arrangements. As financial services become increasingly digital, supervisory attention will continue to focus on fraud and scam risks, as well as emerging risks in anti-money laundering and countering the financing of terrorism (AML/CFT). Preparations for the implementation of the AML Single Rule Book, together with support for the establishment of the European Anti-Money Laundering Authority (AMLA) will also be key areas of focus.

Technology and Digital Change

Technology-driven transformation remains a defining feature of the supervisory landscape, driven by the expanding use of artificial intelligence, digital money and tokenisation across sectors.

The Central Bank will support national implementation of the EU Artificial Intelligence Act (AI Act) and continue developing its supervisory approach to AI use across the financial sector. Supervisory activity will also include authorisation and supervision of crypto-asset service providers under the Markets in Crypto-Assets Regulation (MiCAR), alongside examination of how firms are adapting their business models and managing the risks that come with digital innovation.

Climate and the Long-View

Climate and environmental risks continue to shape the longer-term supervisory agenda. The Central Bank will examine whether climate risk is meaningfully embedded in firms’ governance, risk management and strategic planning, covering both the physical impacts of climate change and the transition risks associated with a move to a low-carbon economy.

What this Means for Firms

The 2026 supervisory agenda points to continued attention on operational resilience and ICT risk management, particularly in the context of DORA. Firms should ensure readiness for the revised Consumer Protection Code, review governance arrangements around AI and emerging technologies, confirm that AML/CFT controls remain aligned with evolving EU reforms and ensure climate risks are appropriately reflected in risk management and business model planning.

Strong governance, effective risk management and clear board oversight remain central to the Central Bank’s expectations across all sectors, including evidence of how firms have embedded the Individual Accountability Framework and SEAR.

How EisnerAmper Ireland can help

EisnerAmper Ireland’s Governance Risk and Compliance team works with regulated firms at every stage of the regulatory lifecycle, from authorisation through to ongoing supervisory engagement. We closely monitor regulatory developments, including the Central Bank’s annual Regulatory and Supervisory Outlook, as part of our commitment to ensuring clients remain informed, prepared and resilient.

If you would like to discuss how the 2026 supervisory priorities impact your firm, please get in touch.

Authors

Are you ready for the amendments to FRS 102?

What is FRS 102 and when is it applied?

Irish company law requires directors of companies incorporated in Ireland to prepare entity financial statements in respect of each financial year. Such financial statements must be prepared either in accordance with:

- International Financial Reporting Standards (‘IFRS’)

IFRS are published by the International Accounting Standards Board (IASB), as adopted by the European Union. Companies with debt or equity securities listed on a regulated EU market are required to be prepared in accordance with IFRS. Commonly large, listed firms or those seeking global investment prepare financial statements under IFRS.

Or as

- Companies Act Financial Statements

These are prepared in accordance with the accounting and disclosure requirements of Irish company law and with the Financial Reporting Standards (‘FRS’) published by the Financial Reporting Council (‘FRC’), the accounting standard setter for both Ireland and the UK. Commonly small and medium sized entities prepare financial statements under FRS 102 as it is less complex to apply than IFRS.

FRS 102, (”FRS102 The Financial Reporting Standard applicable in the UK and Republic of Ireland’) is the principal accounting standard in the Companies Act financial reporting regime. It is largely based on IFRS for SMEs but with significant adaptations for UK & Ireland.

It is subject to periodic review by the FRC. The most recent review in 2024 introduced significant changes which are mandatory for accounting periods beginning on or after 1 January 2026.

What are the updates to FRS 102?

The periodic review 2024 introduces significant amendments to the following sections:

- Section 20 Leases; and

- Section 23 Revenue from Contracts with Customers.

In addition, incremental improvements and clarifications have been made throughout the text of FRS 102 to align the standard with the latest international accounting standards (i.e. IFRS) in certain respects, and to include new and additional guidance to make the requirements easier to understand and apply consistently.

When the amendments are effective

The September 2024 edition of FRS 102 will be mandatory for accounting periods beginning on or after 1 January 2026.

Impact of the amendments to Section 20 Leases

The amendments to Section 20 Leases are based on the principles of IFRS 16 Leases and consequently, for lessees, the distinction between operating and finance leases is removed. This means that the majority of leases will be recognised on-balance sheet.

While lessor accounting remains largely unchanged, the amendments have a significant impact on the recognition, measurement, presentation and disclosure requirements of leases for lessees.

In summary, lessees will be required to:

- Identify lease arrangements by assessing whether a contract is, or contains, a lease.

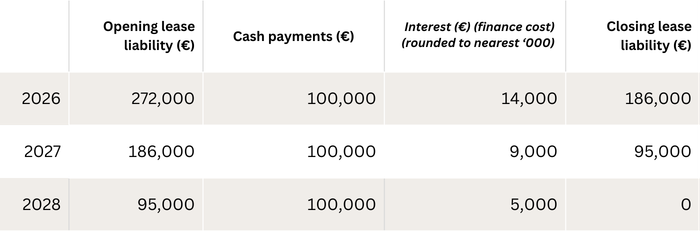

- At the commencement date of the lease, measure the lease liability at the present value of the lease payments that are not paid as at that date. The calculation of the lease liability requires a suitable discount rate with which to discount the relevant cash flows.

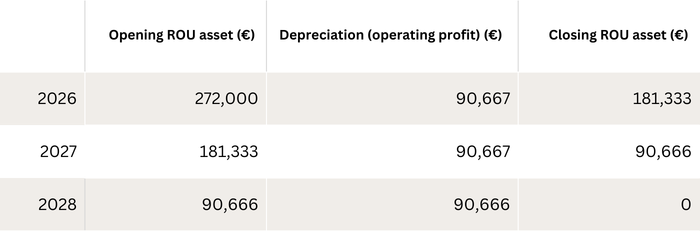

- Measure the right of use (“ROU”) asset at an amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments.

- Depreciate the ROU asset, generally over the life of the lease.

- Accrue interest on the lease liability at the rate implicit in the lease. If that rate cannot be readily determined, the lessee shall choose to apply either the lessee’s incremental borrowing rate or the lessee’s obtainable borrowing rate – to reflect the financing of the ROU asset.

- The discount rate is the periodic rate of interest as described above, the determination of which can take significant judgment.

Illustrative example

Lease term: 3 years

Annual payment payable in arrears: €100,000

Discount rate: 5%

- Indicative present value of ROU asset and lease liability at initial recognition: €272,000. [Present value of lease payments of €100,000 over 3 years at 5%]

Impact of the amendments to Section 23 Revenue from contracts with customers

Section 23 Revenue from Contracts with Customers of FRS 102 was completely rewritten as part of the periodic review 2024 to be based on the principles in IFRS 15 Revenue from Contracts with Customers.

Revenue recognition model

The updated Section 23 replaces the previous risks-and-rewards-based revenue model with a single, principles-based framework focused on the transfer of goods or services to customers, aligning more closely with IFRS 15.

To apply the model, an entity shall take the following steps:

Step 1 – Identify the contract(s) with a customer;

Step 2 – Identify the performance obligations in the contract;

Step 3 – Determine the transaction price;

Step 4 – Allocate the transaction price to the performance obligations in the contract; and

Step 5 – Recognise revenue when (or as) the entity satisfies a performance obligation.

Many contracts will have a single performance obligation. However, when a contract has more than one performance obligation the subsequent steps of the revenue recognition model are designed to ensure that the revenue associated with each performance obligation is recognised at the appropriate time.

There are more disclosure requirements in the new Section 23 which are intended to provide more useful information to users of financial statements about the nature, amount and timing of revenue and cashflows arising from an entity’s contracts with customers.

Entities will need to reassess the accounting treatment of revenue contracts. The application of Section 23 will affect contracts with bundled goods and services, variable consideration, warranties, customer options, financing components and principal vs agent arrangements, as well as obligations satisfied over time.

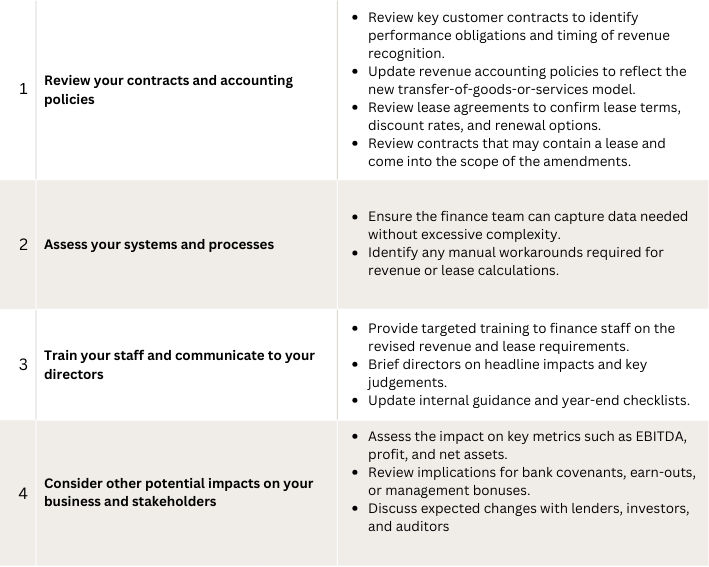

How can you ensure you are prepared for these changes?

To prepare for the amendments, Finance teams should assess how the revised requirements, particularly on revenue recognition and leases, affect existing contracts, accounting policies, systems, and KPIs.

If you would like to have an initial conversation about FRS 102 changes and the potential impacts on your business or if you need specific advice or assistance in respect of the above requirements, feel free to reach out directly. My contact details are as follows: Gavin Redmond on +353 1 2933471 or gavin.redmond@eisneramper.ie

Authors

{kind=link}

Stepping In, Standing Strong: How Interim Expertise can strengthen your Finance Function

In today’s dynamic financial landscape, regulated financial service providers face increasing pressure to maintain financial resilience, regulatory compliance, and strategic clarity – even when unexpected challenges arise. One such challenge is an unexpected absence, vacancy or supplemental resource requirement in the Finance function.

Navigating Uncertainty – How we have helped

At EisnerAmper Ireland (‘EAI’) our Interim Finance Solutions team ensure continuity, confidence, and compliance when resources are needed. Here’s how we’ve supported our clients:

Case Study 1: Immediate Response to an Unexpected Absence

A credit union experienced the sudden departure of its Head of Finance, leaving a gap in leadership and oversight at a crucial time. With no internal successor ready to step in, the board needed urgent support.

We deployed an experienced finance professional to step into the role immediately, working closely with the existing finance team and under the direction of the board. Key outcomes included:

- Ensuring all financial reporting and regulatory submissions were completed on time.

- Identifying and mitigating financial and operational risks.

- Maintaining member and stakeholder confidence during the transition.

This collaborative approach ensured the client remained compliant and operationally stable while planning its next steps

.

Case Study 2: Financial Resource Secondment

EAI is currently appointed as a key financial resource in a bespoke regulated financial services company. Our client elected to engage a secondee resource rather than recruit an in-house resource. Under this arrangement, we provide ongoing support on a ten-day-per-month basis delivering the day-to-day financial management activities of the company.

Our Interim Finance Solution team provides:

- Flexible and experienced financial resource to manage the day-to-day financial activities of the firm.

- Preparation of quarterly management reports and CBI regulatory reports.

- Periodic reporting to the Board on the company’s financial position.

- Preparation of Group Reporting.

Our approach allows the client to ensure adequate controls and processes are in place and ensure continued compliance with regulatory requirements. We continue to support our client in delivering their strategic and regulatory commitments.

Advantages of Interim Financial Support

- Continuity: Keeps financial operations running smoothly during leadership gaps.

- Compliance: Ensures regulatory deadlines and reporting standards are met.

- Confidence: Reassures boards, regulators, and other key stakeholders that financial stewardship is in safe hands.

- Flexibility: Adapts to your businesses size, structure, and strategic needs.

Whether you’re facing an unexpected vacancy or planning a leadership transition, our Interim Finance Solutions team provide the expertise and stability required to keep your business on track. We offer experienced professionals who can step into key roles on a flexible basis ranging from days, weeks or months depending on your needs. Our interim resources provide the necessary skills and expertise to achieve your objectives. Whether it is a short-term gap or a longer-term need our professionals are equipped to add value from day one.

If you have a finance resource requirement, and would like to explore your options, we invite you to contact our team for more information.

Audrey Rigley-Smyth on +353 1 2933477 or audrey.rigley-smyth@eisneramper.ie

Frank Keane on +353 1 2933450 or frank.keane@eisneramper.ie

Authors

Audrey Rigley-Smyth

Director Governance,Risk & Compliance:Risk & Regulatory{kind=link}

Carmanhall Road

Sandyford

Dublin, D18 CA22

Ireland

The content above is provided for general information purposes only and is not intended to provide, nor does it constitute, professional advice on any particular matter. If you would like more information or would like to discuss any of the topics raised above, please contact the author(s).

EisnerAmper Ireland and IADT Launch New Financial Services Management, Governance & Risk Course

EisnerAmper Ireland is pleased to announce that a new Level 9 course, “Financial Services Management, Governance & Risk”, designed in partnership with the Institute of Art, Design and Technology (IADT) has launched.

The course has been developed under the framework of the Memorandum of Understanding entered into between EisnerAmper Ireland and IADT in April 2025 and is designed for those working in or aspiring to work in the financial services sector.

This Level 9 course will equip participants to be critically aware of how to structure effective governance, educate others on managing risk, and be critically aware and technology-enabled to meet future needs.

The launch of this course represents an important milestone in our collaboration with IADT, reflecting our commitment to supporting skills development and innovation within Ireland’s financial services sector.

Industry Expertise at the Core

With tuition from faculty members at IADT and professionals from EisnerAmper Ireland, participants will benefit from real-world insight into governance, regulation, and risk management. Students will engage with executives who work directly with evolving regulatory frameworks and best practices across the sector. Participants will also work with FinReg, the leading development platform for solving Governance, Risk & Compliance (GRC) challenges, reinforcing the programme’s practical and technology-enabled approach.

A Partnership with Purpose

Our partnership with IADT reflects our shared commitment to delivering meaningful, practical, and future-focused learning opportunities. With modules delivered by EisnerAmper Ireland professionals, learners gain access to current market thinking, regulatory context, and hands-on application.

Frank Keane, Partner and member of the Board of EisnerAmper Global said

“The opportunity to collaborate with IADT to design and deliver this programme aligns strongly with our Firm and the EisnerAmper Global network – we are deeply committed to building the right skills to meet the future needs of Ireland’s Financial Services sector.

At EisnerAmper Ireland we are proud of our focus on learning and development at all levels of our Firm. This programme takes that focus to the sector at large and offers a knowledge exchange between our professionals and the sector’s leaders of tomorrow. We are proud to be involved and look forward to learning as much as teaching.”

We look forward to welcoming participants to this innovative programme and to continuing our collaboration with IADT in support of developing the requisite skills that will enable Ireland’s financial services ecosystem to continue to thrive.

Learn more or apply here: https://iadt.ie/courses/financial-services-management-governance-risk/

Learning & Development →EisnerAmper Ireland Academy 2025: Owning Your Art of Practice

Last month, EisnerAmper Ireland hosted our annual EAI Training Academy 2025, part of our Learning and Development programme. The Academy is designed to support our people, build their skills, nurture professional growth, and enhance career development.

This year’s theme, Owning Your Art of Practice, encouraged our team through the lens of our Learning and Development Framework, the ‘Art of Practice’ to reflect on how their individual choices, habits, and daily interactions shape both their professional growth, personal brand and reflects and contributes to EisnerAmper’s brand.

Throughout the day in the tranquil surroundings of Kilruddery House, team members explored key professional development areas, including:

- Defining what each of us wants to be known for and who we want to influence.

- Understanding how the Art of Practice integrates into our day-to-day roles.

- How to use the skills in the Art of Practice through everyday interactions to build strong client relationships, enhance your personal brand which in turn enhances the Firm’s brand.

- Reflecting on personal strengths and decision-making through interactive exercises.

The programme featured two plenary sessions.

The first, ‘Identity, Impact & Influence – A Brand Journey – One Day at a Time’ highlighted the evolution of brands and how individual contributions shape the Firm’s reputation.

Peter Cogan, Managing Partner, Eisner Advisory Group LLC, Eithne Harley, Consultant and former Marketing Director, Accenture, and Diarmaid O’Keeffe, Partner and Head of Audit at EisnerAmper Ireland, shared insights from their experiences as leaders, emphasising the impact of personal visibility, professional choices, and participation in extra-curricular activities.

A series of practitioner-led workshops gave participants practical insights into the nine drivers of the Art of Practice, helping them apply these learning to their current roles and future career paths.

A fireside chat with Michael Doyle, CEO of Ivernia Insurance, focused on career development, personal brand, and professional habits. Michael shared his journey, from early career decisions through to leadership roles, highlighting how consistent choices, continuous learning, and self-awareness contribute to personal and organisational success.

The day concluded with a Johari Window exercise, reinforcing communication, team dynamics, and self-awareness. The Academy 2025 empowered our team to own their own Art of Practice, supporting career growth and strengthening the Firm’s collective expertise. A relaxing team dinner that evening was the perfect end to a great day of reflection and connection.

At EisnerAmper Ireland, we are deeply committed to helping our people learn, grow, and achieve their professional goals.

If you’re looking to build a rewarding career in accounting, audit, advisory or tax, and want to be part of a team that invests in your development, we’d love to hear from you!

Explore our current career opportunities: eisneramper.ie/careers

The Academy →- 1

- 2

- 3

- …

- 40

- →Next Page »

-

Ireland

Our European

head office is

located in Dublin. +353 1 293 3400

+353 1 293 3400

-

Luxembourg

2, Rue Marie Curie

L-8049 Strassen

Luxembourg

-

United States

We have multiple

offices locations across

the United States.

+1 212 949 8700

-

Cayman

Our Central American

office is located in

Grand Cayman.

+1 345 945 5889

-

Singapore

Our Asia office is located in

Singapore.

+65 6305 9900