New Partner Appointments at EisnerAmper Ireland

EisnerAmper Ireland today announced the appointment of Stephen Kinch as Partner, Head of Scaling Services and Siobhan Vickers as Partner, Audit further strengthening the Firm’s senior leadership team.

Stephen Kinch has extensive expertise in scaling high-growth businesses and building agile finance functions to support ambitious expansion plans. He brings practice and senior finance leadership to his role, most recently as CFO of Moby. In his role as Head of Scaling Services, Stephen will lead the continued development of EisnerAmper’s Scaling Services offering, supporting scaling enterprises with finance transformation, fractional CFO and advisory services.

Siobhan joins the Firm with more than 20 years audit experience, leading complex engagements for Irish and multinational companies across the pharmaceutical, technology and hospitality sectors. She previously worked with PWC’s Foreign Direct Investment Group, coordinating large multinational audits across Europe and the US. Her appointment further enhances the Firm’s audit capability and reinforces its commitment to quality, technical excellence and partner-led client service.

Stephen Kinch, Partner, Head of Scaling Servicers, EisnerAmper Ireland, commented:

“I am delighted to join EisnerAmper Ireland at this exciting time for scaling businesses operating from Ireland. Innovation, design thinking and partner led client service are in the DNA of EisnerAmper, this combined with its ability to support organisations across the full finance function makes it a natural choice for growth-focused scaling enterprises.

Access to the EisnerAmper global network further strengthens the proposition for Irish based organisations seeking agile, locally delivered finance leadership. I look forward to working with clients on their scaling journey and to further developing this service within the Firm”.

Siobhan Vickers, Partner, Audit, EisnerAmper Ireland, commented

“EisnerAmper Ireland has built a strong reputation for technical excellence, client service and talent development. It is exceptionally committed to promoting learning and development at all levels. As the profession continues to evolve, firms must prioritise quality management and innovation to deliver effective services and solutions. EisnerAmper is embracing this opportunity.

I am very pleased to be joining such a progressive Firm and look forward to collaborating with my fellow partners and our talented team to continue delivering quality audits for our clients.”

EisnerAmper Ireland CEO, Attracta van Rensburg, commented:

“We are delighted to welcome Stephen and Siobhan to the Firm. These appointments reflect our continued investment in senior leadership capability as part of our long-term growth strategy.

Ireland is exceptionally well positioned as a base for high growth and internationally focused organisations. Under Stephen’s leadership, we are expanding our Scaling Services offering to provide agile fractional CFO and finance advisory solutions tailored to scaling enterprises.

Siobhan’s appointment further strengthens the depth and experience within our Audit practice, reinforcing our commitment to partner-led client service. We are proud to attract senior leaders of this calibre and look forward to the contribution they will make to our Firm and our clients.”

About EisnerAmper Ireland

EisnerAmper Ireland is a specialist firm of accountants, auditors, tax advisors and risk and regulatory experts, with a niche focus on financial services and international trade.

Working alongside 4,000 professionals globally, EisnerAmper Ireland’s 14 Partners and 120+ professionals play a key role in supporting international trade in and through Ireland and in advising Irish corporates.

EisnerAmper Ireland is a founding member of EisnerAmper Global, a New York headquartered specialist network of independent member firms operating across key global international trading and financial services hubs.

Latest News →

Central Bank of Ireland: Key Supervisory Priorities for Credit Unions in 2026

The Central Bank of Ireland (CBI) has published its 2026 Regulatory & Supervisory Outlook (2026 Outlook) outlining the key risks across the financial system and the supervisory priorities that will guide its work in the year ahead. We highlight some of the key cross-sectoral supervisory priorities from the 2026 Outlook here including:

- Resilience under pressure;

- Consumer and Investor protection;

- Technology and digital change;

- Climate and the long-view; and

- What this means for firms.

In relation to Credit Unions, supervisory priorities in 2026 include:

Financial resilience: Reserves and liquidity across the sector remain strong; however, low loan-to-asset ratios continue to present a longer-term sustainability concern. Credit unions availing of the expanded house and business lending framework are expected to do so gradually and prudently. The Central Bank will continue to closely monitor liquidity and asset and liability management (ALM) across the sector.

Business model and strategy: Credit unions are expected to demonstrate progress on digitalisation and sectoral collaboration. Consolidation in the sector, including through transfer of engagements, continues to be encouraged. The Central Bank will progress a regulatory framework for shared service organisations during 2026 and begin policy formulation for corporate credit unions.

Consumer protection, risk management and governance: The revised Consumer Protection Code (CPC) comes into effect in March 2026. The 2026 Outlook notes that the consultation paper on applying the CPC to all regulated credit union activities (CP165) closes in March 2026, with regulations intended to be published by the end of Q3 2026.

In advance of this, the Central Bank expects credit unions to manage conduct risk effectively and demonstrate that members’ interests are protected, while ensuring that risk management frameworks, control environments and operational capabilities continue to mature in line with their product and service offerings and the wider risk environment.

How EisnerAmper Ireland can help

EisnerAmper Ireland’s Governance Risk and Compliance team works with regulated firms at every stage of the regulatory lifecycle, from authorisation through to ongoing supervisory engagement. We closely monitor regulatory developments, including the Central Bank’s annual Regulatory and Supervisory Outlook, as part of our commitment to ensuring clients remain informed, prepared and resilient.

If you would like to discuss how the 2026 supervisory priorities impact your firm, please get in touch.

Authors

Central Bank of Ireland Sets Out Supervisory Priorities for 2026

The Central Bank of Ireland has published its 2026 Regulatory & Supervisory Outlook, outlining the key risks across the financial system and the supervisory priorities that will guide its work in the year ahead.

This is the third year of the report, which is framed against a “rapidly changing international environment characterised by geopolitical tensions, macro-financial uncertainty, technological disruption and climate transition.” While the financial system is described as resilient, the emphasis is on sustaining that resilience through strong governance, effective risk management and operational preparedness.

For regulated firms, the overarching message is clear: regulatory frameworks must be fully embedded and sufficiently robust to respond to this increasingly complex risk landscape.

Below we highlight some of the key cross-sectoral supervisory priorities from the 2026 Outlook:

Resilience Under Pressure

Operational and cyber risks remain central supervisory priorities. The Central Bank highlights the elevated risk environment arising from increasing operational complexity, accelerating digitalisation and firms’ reliance on critical third-party ICT providers.

In 2026, supervisory engagement will include Digital Operational Resilience Act (DORA) implementation, with particular reference to gaps identified in ICT risk management frameworks, governance, third-party oversight and incident reporting practices. Supervisory scrutiny will continue to centre on firms’ preparedness for operational disruption and the ability to maintain continuity of critical services.

From a financial resilience perspective, supervisory focus will remain on credit, liquidity, market stability alongside the sustainability of underlying business models. The report also highlights the growing significance of non-bank financial institutions and interconnected market exposures within the broader risk landscape.

Consumer and Investor Protection

Consumer and investor protection remains central to the supervisory agenda. The revised Consumer Protection Code (CPC), effective from March 2026, will form a central component of supervisory engagement across sectors.

Supervisory work will examine firms’ day-to-day treatment of customers, including complaints handling, management of conflicts of interest, the quality and clarity of client disclosures and products’ governance arrangements. As financial services become increasingly digital, supervisory attention will continue to focus on fraud and scam risks, as well as emerging risks in anti-money laundering and countering the financing of terrorism (AML/CFT). Preparations for the implementation of the AML Single Rule Book, together with support for the establishment of the European Anti-Money Laundering Authority (AMLA) will also be key areas of focus.

Technology and Digital Change

Technology-driven transformation remains a defining feature of the supervisory landscape, driven by the expanding use of artificial intelligence, digital money and tokenisation across sectors.

The Central Bank will support national implementation of the EU Artificial Intelligence Act (AI Act) and continue developing its supervisory approach to AI use across the financial sector. Supervisory activity will also include authorisation and supervision of crypto-asset service providers under the Markets in Crypto-Assets Regulation (MiCAR), alongside examination of how firms are adapting their business models and managing the risks that come with digital innovation.

Climate and the Long-View

Climate and environmental risks continue to shape the longer-term supervisory agenda. The Central Bank will examine whether climate risk is meaningfully embedded in firms’ governance, risk management and strategic planning, covering both the physical impacts of climate change and the transition risks associated with a move to a low-carbon economy.

What this Means for Firms

The 2026 supervisory agenda points to continued attention on operational resilience and ICT risk management, particularly in the context of DORA. Firms should ensure readiness for the revised Consumer Protection Code, review governance arrangements around AI and emerging technologies, confirm that AML/CFT controls remain aligned with evolving EU reforms and ensure climate risks are appropriately reflected in risk management and business model planning.

Strong governance, effective risk management and clear board oversight remain central to the Central Bank’s expectations across all sectors, including evidence of how firms have embedded the Individual Accountability Framework and SEAR.

How EisnerAmper Ireland can help

EisnerAmper Ireland’s Governance Risk and Compliance team works with regulated firms at every stage of the regulatory lifecycle, from authorisation through to ongoing supervisory engagement. We closely monitor regulatory developments, including the Central Bank’s annual Regulatory and Supervisory Outlook, as part of our commitment to ensuring clients remain informed, prepared and resilient.

If you would like to discuss how the 2026 supervisory priorities impact your firm, please get in touch.

Authors

Are you ready for the amendments to FRS 102?

What is FRS 102 and when is it applied?

Irish company law requires directors of companies incorporated in Ireland to prepare entity financial statements in respect of each financial year. Such financial statements must be prepared either in accordance with:

- International Financial Reporting Standards (‘IFRS’)

IFRS are published by the International Accounting Standards Board (IASB), as adopted by the European Union. Companies with debt or equity securities listed on a regulated EU market are required to be prepared in accordance with IFRS. Commonly large, listed firms or those seeking global investment prepare financial statements under IFRS.

Or as

- Companies Act Financial Statements

These are prepared in accordance with the accounting and disclosure requirements of Irish company law and with the Financial Reporting Standards (‘FRS’) published by the Financial Reporting Council (‘FRC’), the accounting standard setter for both Ireland and the UK. Commonly small and medium sized entities prepare financial statements under FRS 102 as it is less complex to apply than IFRS.

FRS 102, (”FRS102 The Financial Reporting Standard applicable in the UK and Republic of Ireland’) is the principal accounting standard in the Companies Act financial reporting regime. It is largely based on IFRS for SMEs but with significant adaptations for UK & Ireland.

It is subject to periodic review by the FRC. The most recent review in 2024 introduced significant changes which are mandatory for accounting periods beginning on or after 1 January 2026.

What are the updates to FRS 102?

The periodic review 2024 introduces significant amendments to the following sections:

- Section 20 Leases; and

- Section 23 Revenue from Contracts with Customers.

In addition, incremental improvements and clarifications have been made throughout the text of FRS 102 to align the standard with the latest international accounting standards (i.e. IFRS) in certain respects, and to include new and additional guidance to make the requirements easier to understand and apply consistently.

When the amendments are effective

The September 2024 edition of FRS 102 will be mandatory for accounting periods beginning on or after 1 January 2026.

Impact of the amendments to Section 20 Leases

The amendments to Section 20 Leases are based on the principles of IFRS 16 Leases and consequently, for lessees, the distinction between operating and finance leases is removed. This means that the majority of leases will be recognised on-balance sheet.

While lessor accounting remains largely unchanged, the amendments have a significant impact on the recognition, measurement, presentation and disclosure requirements of leases for lessees.

In summary, lessees will be required to:

- Identify lease arrangements by assessing whether a contract is, or contains, a lease.

- At the commencement date of the lease, measure the lease liability at the present value of the lease payments that are not paid as at that date. The calculation of the lease liability requires a suitable discount rate with which to discount the relevant cash flows.

- Measure the right of use (“ROU”) asset at an amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments.

- Depreciate the ROU asset, generally over the life of the lease.

- Accrue interest on the lease liability at the rate implicit in the lease. If that rate cannot be readily determined, the lessee shall choose to apply either the lessee’s incremental borrowing rate or the lessee’s obtainable borrowing rate – to reflect the financing of the ROU asset.

- The discount rate is the periodic rate of interest as described above, the determination of which can take significant judgment.

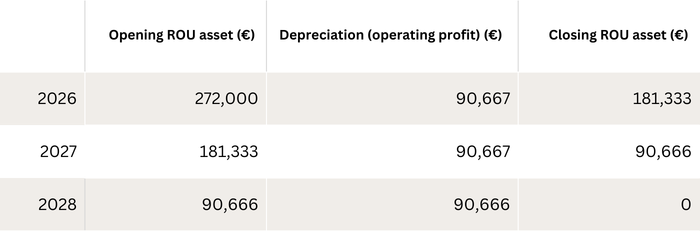

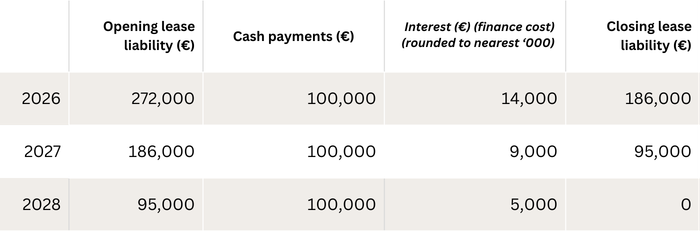

Illustrative example

Lease term: 3 years

Annual payment payable in arrears: €100,000

Discount rate: 5%

- Indicative present value of ROU asset and lease liability at initial recognition: €272,000. [Present value of lease payments of €100,000 over 3 years at 5%]

Impact of the amendments to Section 23 Revenue from contracts with customers

Section 23 Revenue from Contracts with Customers of FRS 102 was completely rewritten as part of the periodic review 2024 to be based on the principles in IFRS 15 Revenue from Contracts with Customers.

Revenue recognition model

The updated Section 23 replaces the previous risks-and-rewards-based revenue model with a single, principles-based framework focused on the transfer of goods or services to customers, aligning more closely with IFRS 15.

To apply the model, an entity shall take the following steps:

Step 1 – Identify the contract(s) with a customer;

Step 2 – Identify the performance obligations in the contract;

Step 3 – Determine the transaction price;

Step 4 – Allocate the transaction price to the performance obligations in the contract; and

Step 5 – Recognise revenue when (or as) the entity satisfies a performance obligation.

Many contracts will have a single performance obligation. However, when a contract has more than one performance obligation the subsequent steps of the revenue recognition model are designed to ensure that the revenue associated with each performance obligation is recognised at the appropriate time.

There are more disclosure requirements in the new Section 23 which are intended to provide more useful information to users of financial statements about the nature, amount and timing of revenue and cashflows arising from an entity’s contracts with customers.

Entities will need to reassess the accounting treatment of revenue contracts. The application of Section 23 will affect contracts with bundled goods and services, variable consideration, warranties, customer options, financing components and principal vs agent arrangements, as well as obligations satisfied over time.

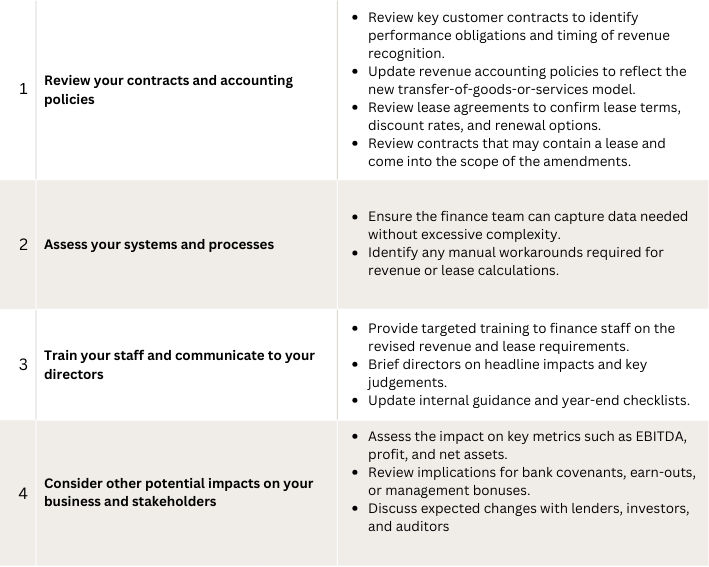

How can you ensure you are prepared for these changes?

To prepare for the amendments, Finance teams should assess how the revised requirements, particularly on revenue recognition and leases, affect existing contracts, accounting policies, systems, and KPIs.

If you would like to have an initial conversation about FRS 102 changes and the potential impacts on your business or if you need specific advice or assistance in respect of the above requirements, feel free to reach out directly. My contact details are as follows: Gavin Redmond on +353 1 2933471 or gavin.redmond@eisneramper.ie

Authors

Stepping In, Standing Strong: How Interim Expertise can strengthen your Finance Function

In today’s dynamic financial landscape, regulated financial service providers face increasing pressure to maintain financial resilience, regulatory compliance, and strategic clarity – even when unexpected challenges arise. One such challenge is an unexpected absence, vacancy or supplemental resource requirement in the Finance function.

Navigating Uncertainty – How we have helped

At EisnerAmper Ireland (‘EAI’) our Interim Finance Solutions team ensure continuity, confidence, and compliance when resources are needed. Here’s how we’ve supported our clients:

Case Study 1: Immediate Response to an Unexpected Absence

A credit union experienced the sudden departure of its Head of Finance, leaving a gap in leadership and oversight at a crucial time. With no internal successor ready to step in, the board needed urgent support.

We deployed an experienced finance professional to step into the role immediately, working closely with the existing finance team and under the direction of the board. Key outcomes included:

- Ensuring all financial reporting and regulatory submissions were completed on time.

- Identifying and mitigating financial and operational risks.

- Maintaining member and stakeholder confidence during the transition.

This collaborative approach ensured the client remained compliant and operationally stable while planning its next steps

.

Case Study 2: Financial Resource Secondment

EAI is currently appointed as a key financial resource in a bespoke regulated financial services company. Our client elected to engage a secondee resource rather than recruit an in-house resource. Under this arrangement, we provide ongoing support on a ten-day-per-month basis delivering the day-to-day financial management activities of the company.

Our Interim Finance Solution team provides:

- Flexible and experienced financial resource to manage the day-to-day financial activities of the firm.

- Preparation of quarterly management reports and CBI regulatory reports.

- Periodic reporting to the Board on the company’s financial position.

- Preparation of Group Reporting.

Our approach allows the client to ensure adequate controls and processes are in place and ensure continued compliance with regulatory requirements. We continue to support our client in delivering their strategic and regulatory commitments.

Advantages of Interim Financial Support

- Continuity: Keeps financial operations running smoothly during leadership gaps.

- Compliance: Ensures regulatory deadlines and reporting standards are met.

- Confidence: Reassures boards, regulators, and other key stakeholders that financial stewardship is in safe hands.

- Flexibility: Adapts to your businesses size, structure, and strategic needs.

Whether you’re facing an unexpected vacancy or planning a leadership transition, our Interim Finance Solutions team provide the expertise and stability required to keep your business on track. We offer experienced professionals who can step into key roles on a flexible basis ranging from days, weeks or months depending on your needs. Our interim resources provide the necessary skills and expertise to achieve your objectives. Whether it is a short-term gap or a longer-term need our professionals are equipped to add value from day one.

If you have a finance resource requirement, and would like to explore your options, we invite you to contact our team for more information.

Audrey Rigley-Smyth on +353 1 2933477 or audrey.rigley-smyth@eisneramper.ie

Frank Keane on +353 1 2933450 or frank.keane@eisneramper.ie

Authors

Audrey Rigley-Smyth

Director Governance,Risk & Compliance:Risk & RegulatoryCarmanhall Road

Sandyford

Dublin, D18 CA22

Ireland

The content above is provided for general information purposes only and is not intended to provide, nor does it constitute, professional advice on any particular matter. If you would like more information or would like to discuss any of the topics raised above, please contact the author(s).

EisnerAmper Ireland and IADT Launch New Financial Services Management, Governance & Risk Course

EisnerAmper Ireland is pleased to announce that a new Level 9 course, “Financial Services Management, Governance & Risk”, designed in partnership with the Institute of Art, Design and Technology (IADT) has launched.

The course has been developed under the framework of the Memorandum of Understanding entered into between EisnerAmper Ireland and IADT in April 2025 and is designed for those working in or aspiring to work in the financial services sector.

This Level 9 course will equip participants to be critically aware of how to structure effective governance, educate others on managing risk, and be critically aware and technology-enabled to meet future needs.

The launch of this course represents an important milestone in our collaboration with IADT, reflecting our commitment to supporting skills development and innovation within Ireland’s financial services sector.

Industry Expertise at the Core

With tuition from faculty members at IADT and professionals from EisnerAmper Ireland, participants will benefit from real-world insight into governance, regulation, and risk management. Students will engage with executives who work directly with evolving regulatory frameworks and best practices across the sector. Participants will also work with FinReg, the leading development platform for solving Governance, Risk & Compliance (GRC) challenges, reinforcing the programme’s practical and technology-enabled approach.

A Partnership with Purpose

Our partnership with IADT reflects our shared commitment to delivering meaningful, practical, and future-focused learning opportunities. With modules delivered by EisnerAmper Ireland professionals, learners gain access to current market thinking, regulatory context, and hands-on application.

Frank Keane, Partner and member of the Board of EisnerAmper Global said

“The opportunity to collaborate with IADT to design and deliver this programme aligns strongly with our Firm and the EisnerAmper Global network – we are deeply committed to building the right skills to meet the future needs of Ireland’s Financial Services sector.

At EisnerAmper Ireland we are proud of our focus on learning and development at all levels of our Firm. This programme takes that focus to the sector at large and offers a knowledge exchange between our professionals and the sector’s leaders of tomorrow. We are proud to be involved and look forward to learning as much as teaching.”

We look forward to welcoming participants to this innovative programme and to continuing our collaboration with IADT in support of developing the requisite skills that will enable Ireland’s financial services ecosystem to continue to thrive.

Learn more or apply here: https://iadt.ie/courses/financial-services-management-governance-risk/

Learning & Development →EisnerAmper Ireland Academy 2025: Owning Your Art of Practice

Last month, EisnerAmper Ireland hosted our annual EAI Training Academy 2025, part of our Learning and Development programme. The Academy is designed to support our people, build their skills, nurture professional growth, and enhance career development.

This year’s theme, Owning Your Art of Practice, encouraged our team through the lens of our Learning and Development Framework, the ‘Art of Practice’ to reflect on how their individual choices, habits, and daily interactions shape both their professional growth, personal brand and reflects and contributes to EisnerAmper’s brand.

Throughout the day in the tranquil surroundings of Kilruddery House, team members explored key professional development areas, including:

- Defining what each of us wants to be known for and who we want to influence.

- Understanding how the Art of Practice integrates into our day-to-day roles.

- How to use the skills in the Art of Practice through everyday interactions to build strong client relationships, enhance your personal brand which in turn enhances the Firm’s brand.

- Reflecting on personal strengths and decision-making through interactive exercises.

The programme featured two plenary sessions.

The first, ‘Identity, Impact & Influence – A Brand Journey – One Day at a Time’ highlighted the evolution of brands and how individual contributions shape the Firm’s reputation.

Peter Cogan, Managing Partner, Eisner Advisory Group LLC, Eithne Harley, Consultant and former Marketing Director, Accenture, and Diarmaid O’Keeffe, Partner and Head of Audit at EisnerAmper Ireland, shared insights from their experiences as leaders, emphasising the impact of personal visibility, professional choices, and participation in extra-curricular activities.

A series of practitioner-led workshops gave participants practical insights into the nine drivers of the Art of Practice, helping them apply these learning to their current roles and future career paths.

A fireside chat with Michael Doyle, CEO of Ivernia Insurance, focused on career development, personal brand, and professional habits. Michael shared his journey, from early career decisions through to leadership roles, highlighting how consistent choices, continuous learning, and self-awareness contribute to personal and organisational success.

The day concluded with a Johari Window exercise, reinforcing communication, team dynamics, and self-awareness. The Academy 2025 empowered our team to own their own Art of Practice, supporting career growth and strengthening the Firm’s collective expertise. A relaxing team dinner that evening was the perfect end to a great day of reflection and connection.

At EisnerAmper Ireland, we are deeply committed to helping our people learn, grow, and achieve their professional goals.

If you’re looking to build a rewarding career in accounting, audit, advisory or tax, and want to be part of a team that invests in your development, we’d love to hear from you!

Explore our current career opportunities: eisneramper.ie/careers

Learning & Development →Navigating a Central Bank Risk Mitigation Programme: A Practical Guide

The Central Bank of Ireland (Central Bank) takes an outcome focused, risk-based approach to supervision as outlined in their “Our Approach to Supervision”, which was published alongside its Regulatory & Supervisory Outlook Report 2025.

RMP’s are part of the Central Bank’s Supervisory Toolkit and may be used as an intervention arising from their supervision.

If you are a Board Chair, CEO, or other senior executive who has received a RMP you may be trying to understand how to respond effectively which is critical, not only to meet regulatory expectations but also to safeguard your organisations reputation and resilience.

Drawing on years of experience advising boards and executive teams, we’ve developed a practical framework to help leaders like you navigate the RMP process with confidence and clarity. In this article, I’ll outline key steps to take, common pitfalls to avoid, and how to turn regulatory scrutiny into an opportunity for strengthening governance and risk management.

Why is Supervision necessary?

Financial regulation is important and necessary, but, on its own, it is not enough to protect members, consumers and investors, keep firms safe and stable, maintain trust in the financial system, and support overall financial stability, i.e. the Central Bank’s Safeguarding Outcomes.

That’s why supervision is also essential. Supervision means the Central Bank will actively work with financial firms, analysing their activities and keeping a close watch to make sure that regulations are followed and risks are mitigated. This approach ensures that not only are regulations put into practice, but the support is there to check that they are working as intended, and action is taken when they are not.

By taking an outcome focused, risk-based approach the Central Bank can communicate its supervisory concerns to sectors and firms and highlight the outcomes expected and the timelines for them to be achieved.

Why does the Central Bank issue a Risk Mitigation Programme (RMP)?

If a firm is found to have issues or concerns in high-risk areas, for example, poor governance, weak financial controls, or inadequate third-party risk management, the Central Bank may issue a Risk Mitigation Programme (RMP). A RMP is a formal set of actions a regulated firm must take to fix those issues. It includes:

- What needs to be done.

- Who is responsible.

- When it must be completed.

This helps ensure the firm:

- Protects its members, customers and investors.

- Stays financially sound.

- Maintains trust in the financial system.

- Supports overall financial stability.

When might an RMP be issued?

A RMP may be issued:

- After a supervisory review or inspection.

- If the firm’s regulatory risk profile increases.

- When there are concerns about compliance, resilience or governance.

- If the firm’s actions could impact on the wider financial system.

How to respond to the Central Bank’s Risk Mitigation Programme?

Outcome focused and risk-based supervision remains fundamental to the Central Bank’s approach and any supervisory concerns will be communicated to sectors and firms. This may take the form of, for example, a ‘Dear CEO/Chair” letter, issuance of a risk mitigation programme (RMP) requiring a firm to prepare a skilled report, or at the higher end of the Central Bank’s escalation toolkit, the utilisation of direction-making powers, including enforcement actions. Firms must ensure they take appropriate risk mitigation actions to address the issues identified and the desired outcomes expected. Set out below is a practical framework to help you navigate the RMP process:

- Carefully review the RMP letter – it will outline the specific weaknesses identified, the required actions, desired outcomes and the deadlines.

- Engage and Clarify – if you are unclear about any part of the RMP, engage your Central Bank supervisor for clarification.

- Conduct a Gap Analysis – compare the Central Bank’s expectations with your current frameworks, policies and practices. Focus on the Central Bank’s identified weaknesses and desired outcomes in addition to regulatory requirements, guidance and best practices.

- Identify areas where your firm falls short and need enhancement.

- Develop a comprehensive remediation plan.

- Assign responsibilities.

- Board – Clearly communicate to the Board what their responsibilities are in respect of the RMP.

- Project Manager – assign a project manager responsible for planning, executing and closing the project considering the weaknesses identified, regulatory compliance. requirements, the Central Bank’s expected outcomes together with internal and external timelines.

- Action Owners – ensure detailed actions have a clear owner within the business to drive the remediation actions in line with desired outcomes.

- Set internal deadlines – that will ensure that internal reviews and reporting requirements are met in advance of the Central Bank’s deadlines to allow for review and adjustments.

- Document everything – maintain a clear audit trail of decisions, actions and communications.

- Ensure the issues and concerns – identified by the Central Bank in the RMP letter are appropriately strengthened via the remediation actions identified in your plan and are aligned with regulatory requirements and the Central Bank’s desired outcomes.

- Develop a comprehensive remediation project management cadence:

- Ensure there are internal structures for progressing the remediation plan including regular project touch points and regular internal progress reporting.

- Provide regular updates to the Central Bank on progress and where required submit evidence of the remediation progress which may include, for example, evidence of updates to policies, training records, system changes or audit results.

- Should you hit a roadblock or need more time, communicate early and clearly with the Central Bank. Be transparent about challenges or delays and propose realistic solutions. Transparency builds trust.

- Make sure responses are well-supported, accurate and aligned with regulatory expectations.

- Embed the Central Bank’s desired outcomes – into your systems and controls and ensure it is aligned with identified weaknesses, regulatory requirements, guidance, best practices and the Central Bank’s desired outcome.

- Be prepared for a follow-up. The Central Bank may undertake a follow-up inspection or request additional documentation.

- Be ready to demonstrate – how changes have been embedded and made operational in addition to how they are monitored and overseen to reinforce the changes and avoid further risk

If you are a Board Chair, CEO or other senior executive who has received a RMP and would like to talk through how you can best organise your team to respond to it, I’m happy to have a conversation with you, on a no obligations basis, to help guide you on those first steps.

Feel free to reach out directly my contact details are as follows: Carina Myles on +353 1 293346 or carina.myles@eisneramper.ie

Authors

EisnerAmper Ireland Opens Ireland West Office in Sligo

EisnerAmper Ireland are delighted to announce the establishment of our Ireland West office and welcome a talented group of professionals who have joined us as we establish our presence in Sligo.

Having an office in Sligo provides us with a greater opportunity to connect with our clients based outside the capital. Sligo also offers a unique blend of professional opportunity and quality of life, making it an ideal location for our expansion, offering staff an alternative location to our Dublin office.

While our permanent Sligo office is currently under development on Stephen Street our team will be located on the campus of Atlantic Technological University. As a hub of talent attraction, education, and retention, the ATU is a welcoming home for our team. This expansion allows us to continue developing exceptional practitioners equipped with the tools capable of delivering the highest quality outcome to our clients.

Our presence in Sligo marks an exciting step in EisnerAmper Ireland’s journey and reflects our focus on investing in people, regions, and the future of professional services in Ireland.

We look forward to becoming an active part of the Sligo business and academic community.

Latest News →EisnerAmper Ireland Welcomes Their 2025 Graduate Trainees

We are delighted to welcome the newest members of our team as part of the EisnerAmper Ireland Graduate Programme 2025.

Our new trainees completed a comprehensive two-week on-site Induction Programme, covering technical training, practical on-the-job experience, and soft skills development. They also gained exposure to our Audit, Accounting & Compliance, and Tax departments.

The EisnerAmper Ireland Graduate Programme is different – from day one, our trainees work alongside Partners and senior management, gaining hands-on experience and building the knowledge, skills, and confidence to develop as a practitioner.

If you are looking to start your career in audit, accountancy, or tax with real-world experience at a firm that values and nurtures dedication and commitment, our Graduate Programme 2026 could be the perfect fit.

Learn more here: https://eisneramper.ie/graduate-programme-join-our-firm/

Latest News →EisnerAmper Ireland Summer Get-Together 2025

In the closing days of Summer 2025 the EisnerAmper Ireland team came together for our annual Summer Party at the Horse Show House Pub.

It was a fantastic afternoon allowing us to relax, connect, and celebrate together outside the office. Events like these are a great reminder that while we work hard, we also take the time to enjoy shared experiences as a team.

A big thank you to everyone who joined us and helped make the evening such a success! We look forward to many more celebrations ahead!

EisnerAmper Ireland Hosts second Discovery Afternoon for Villanova University

On May 13, we were delighted to welcome the 2025 Maymester students from Villanova University to our second EisnerAmper Ireland Discovery Afternoon, a unique, immersive experience designed to share what it means to be a Professional in Practice.

Tailored specifically for students considering careers in accounting, advisory and consulting, the afternoon offered a deep dive into our Firm’s values, culture, structure, and strategic approach. Most importantly, it gave students the opportunity to hear from professionals at all stages of their careers, from trainee to CEO.

Our guests were welcomed by Attracta van Rensburg, CEO of EisnerAmper Ireland, who opened the afternoon by outlining the purpose of the session: to provide meaningful insights into the world of professional services, to demonstrate our people-first approach to development, and to highlight how innovation, design thinking and technology are at the heart of our client service delivery.

Understanding EisnerAmper Ireland’s DNA

Frank Keane, Partner Risk & Regulatory and Board Member of EisnerAmper Global, gave an overview of EisnerAmper Ireland’s position within the EisnerAmper Global network. He walked students through our Firm’s journey, from our beginnings in 2005 as MKO Partners, to the launch of EisnerAmper Global in 2015, to our strategic evolution from a traditional service-based offering to a combined services and solutions model with a niche market focus.

Frank also shared personal reflections on professionalism, ethics, and purpose in practice, sparking conversations on what it means to be a values-driven professional in today’s dynamic and regulated business environment.

People & Pathways: From Graduate to Practitioner

Our HR team, Laura Cowman, Director and Jen Higgins, Manager, introduced students to our Graduate Programme, providing a practical overview of training, career pathways, and the support available to new joiners.

This was followed by an authentic and relatable session featuring Alex O’Meara, a current Intern, and Leanne Mulderrig, a Supervisor. Both shared their personal journeys with EisnerAmper Ireland, from the learning curve of starting out to stepping into leadership and mentorship roles, giving students a real sense of what life is like inside a high-performing, people-focused firm.

Innovation in Action: EA Solve

Students were then introduced to EA Solve, our dedicated solutions division. Joseph Halligan, Manager, and Johnatan Epure, Solutions Builder, led an engaging session on how EA Solve delivers value across a wide range of industries by combining subject matter expertise, cutting-edge technology, and a dynamic, agile approach to problem-solving.

They provided an overview of EA Solve’s innovative operating model, outlining how we approach product development and delivery, from identifying client needs to creating scalable solutions that drive results. To bring this to life, students were given a live demonstration of CU Risk Core, a bespoke risk management system developed specifically for Risk Officers in Irish Credit Unions.

Far from simply responding to change, EA Solve is designed to set the pace, helping clients productise services, solve complex challenges, and operate more efficiently. The session illustrated how innovation at EisnerAmper Ireland isn’t just a concept, but a core strategy embedded in how we think, build, and deliver lasting impact.

ESG & the Future of Reporting

Later in the afternoon, Frank returned to lead a session on Sustainability and ESG Reporting, with a particular focus on developments in the European Union, such as the Corporate Sustainability Reporting Directive (CSRD) and its current iteration.

He explored both the complexities and opportunities these new regulations and their “voluntary” equivalents present for organisations, from data challenges to investor expectations, and he emphasised the growing importance of ESG as a strategic business driver. The session sparked thoughtful questions from the students, including a debate on the sustainability of artificial intelligence itself, highlighting their curiosity and engagement with contemporary business issues.

Fireside Chat with Troy Lavin, VitHit

The afternoon culminated in a fireside chat between Frank Keane and Troy Lavin, Managing Director of VitHit, one of Ireland’s most successful wellness beverage brands. Troy spoke candidly about the entrepreneurial journey, from branding and product development to navigating global markets and underscored the importance of resilience, innovation, and financial discipline.

We concluded the day with refreshments and informal networking in The Bank on College Green, giving students the opportunity to connect further with our team, ask questions, and reflect on the day’s insights.

We would like to extend a sincere thank you to all our speakers and to the Villanova University students for their energy and curiosity. We’re passionate about helping future professionals discover how they can make a meaningful impact, and we look forward to welcoming the next cohort in 2026!

Learning & Development →- 1

- 2

- 3

- …

- 39

- →Next Page »

{kind=link}

{kind=link}

;){kind=link}